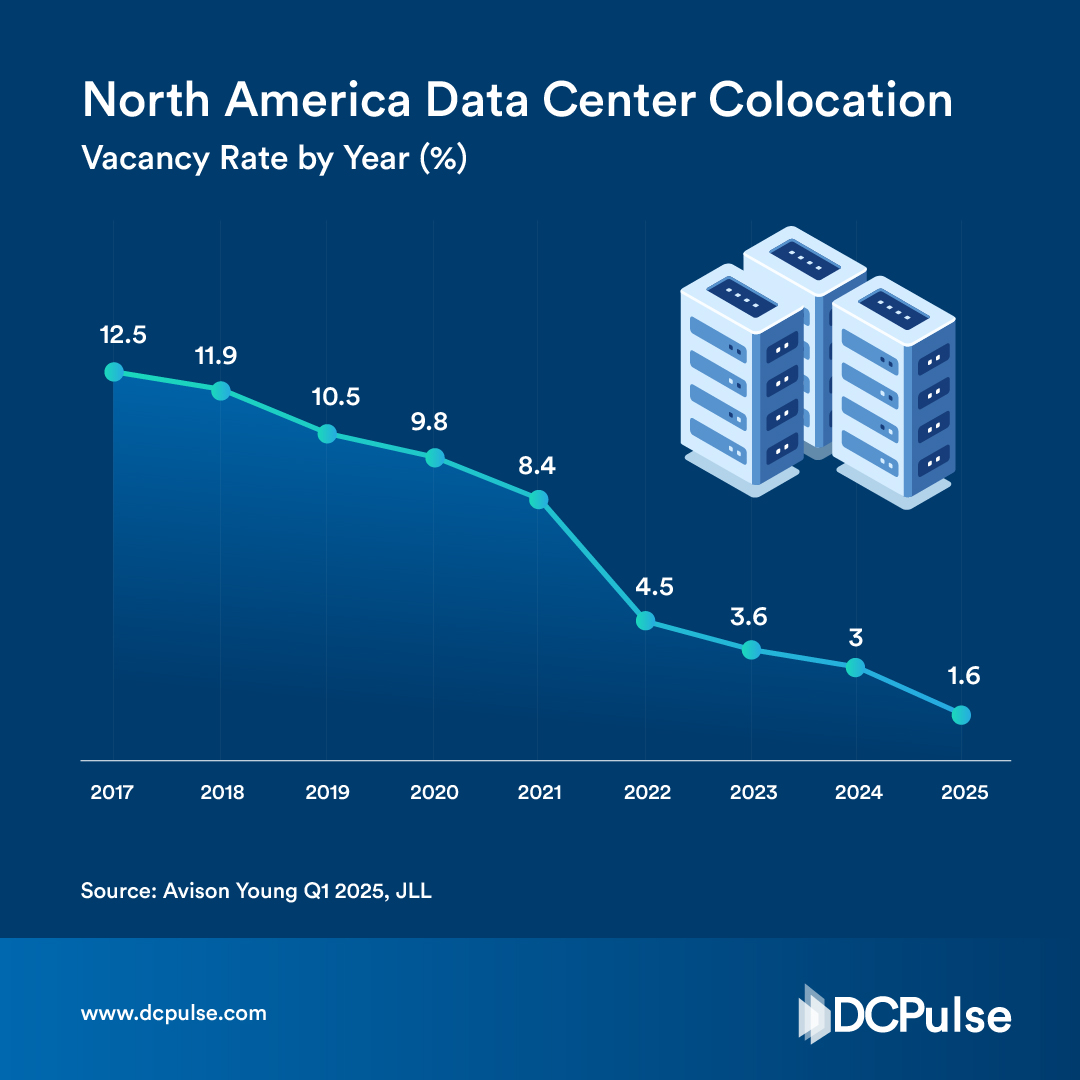

Vacancy rates in North American data centers have hit record lows which is evident from the availability of approximately 1.6% of space in the U.S., as of 2025, thereby hampering the space availability for large areas over 5 MW, where the second-generation space is typically rented out in a short span (typically a few weeks) leading to a highly constrained market where large-scale tenants face long wait times and intense competition for available capacity.

Despite the development of approximately 6.5 GW space across North America, nearly 72% space has witnessed pre-booking, eventually forcing major data center operators to reserve space years in advance and eventually limiting the ability of the data center sector to scale in response to growing demand.

The shortage of space coupled with availability of power to run the data center facilities acts as a major barrier to the growth of the data center industry, disrupting the influx of leading industry players to the region.

The space crunch has developed as a result of the decade-long real estate vacancy unavailability problem which is evident from the sharp decline in the U.S. vacancy rates from 12.5% in 2017 to 9.8% in 2020, before reaching the current record low.

The consistent drop underscores the surging demand for digital infrastructure driven primarily by the rapid adoption of cloud computing, growth of Artificial Intelligence (AI), and expansion of hyperscale facilities across the U.S. leading to outpace of new supply.