Not long ago, choosing a colocation data center was a relatively straightforward decision. You needed space, power, connectivity, and a reasonable price. You compared a handful of colocation data center providers, picked the one closest to your office or your customers, signed a contract, and moved on. The facility itself was largely invisible, a utility, not a differentiator.

That calculus has fundamentally changed. Today, the right AI colocation facility, one engineered for high-density AI workloads, liquid cooling, and GPU-scale power delivery, is not just a place to put servers. It is a strategic asset. And the wrong one can quietly become a ceiling on everything your business is trying to build.

How Has the Colocation Market Changed, and Why Is AI the Turning Point?

What is a colocation data center? At its core, it is a shared facility where businesses rent space, power, and connectivity to house their own servers and networking equipment, without the capital commitment of building and operating their own infrastructure. For years, that model was defined by reliability, location, and price. Today, a fourth dimension has entered the equation: AI readiness.

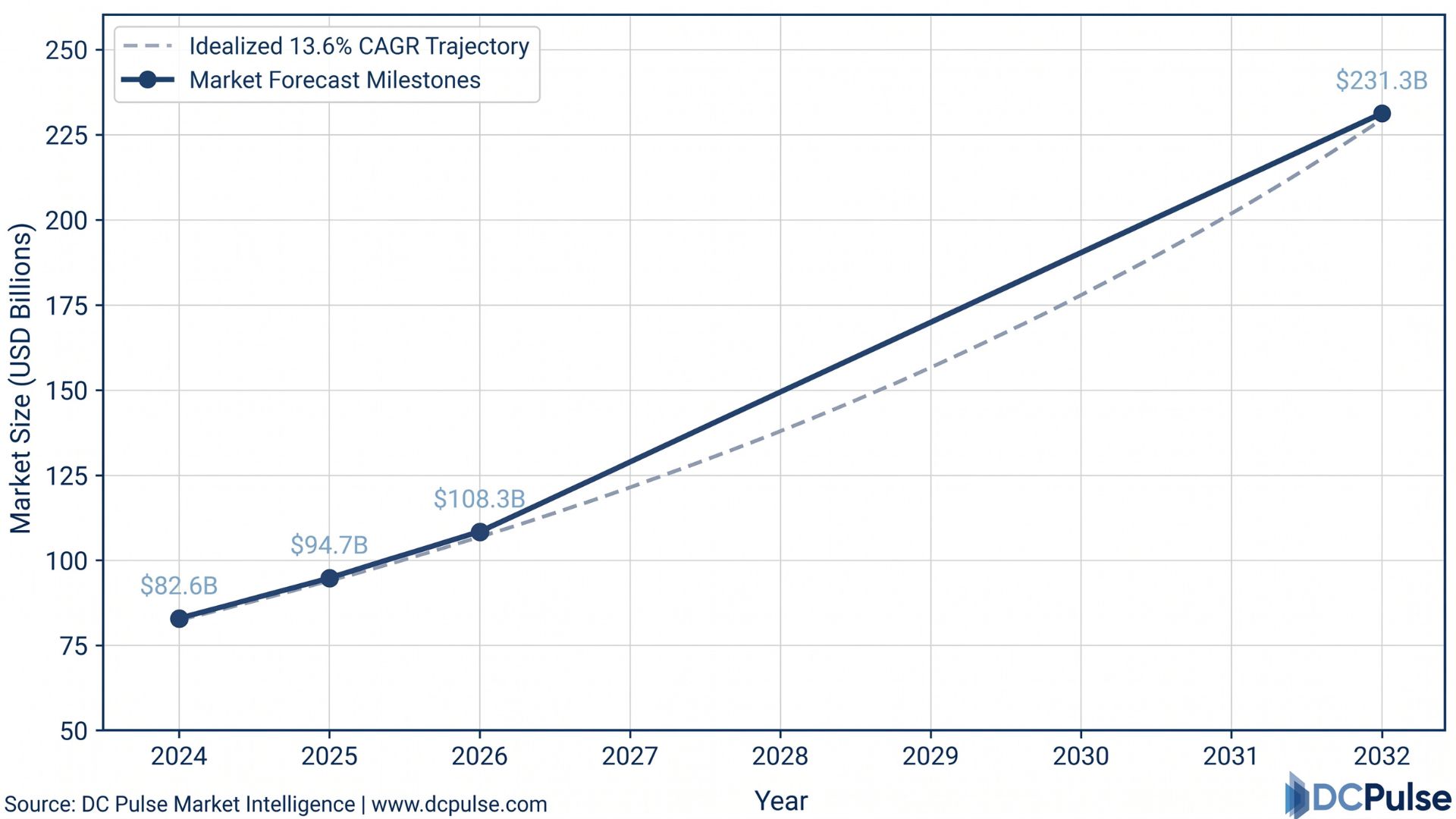

The shift is structural, not cyclical. The global data center colocation market stood at USD 94.7 billion in 2025 and is forecast to reach Usd 108.3 billion in 2026, a 14.4% year-on-year increase. The colocation data center segment of the AI data center market is expected to register the highest CAGR of 32.6% through 2032, significantly outpacing every other segment. The demand driving those numbers is not general cloud growth; it is AI workloads requiring high-density colocation infrastructure that traditional facilities were never designed to support.

Global Data Center Colocation Market Trajectory (2024-2032)

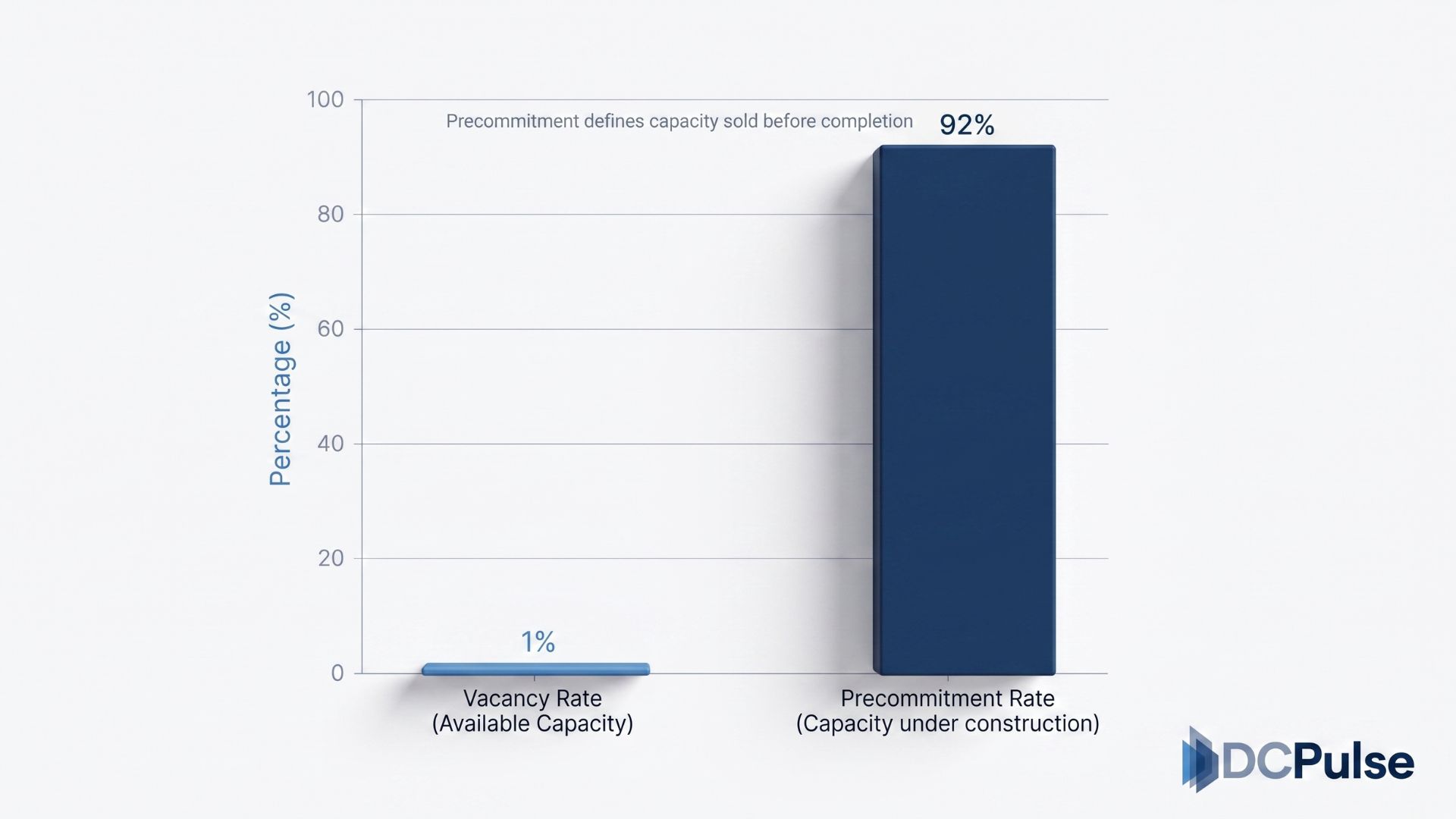

The supply side tells an equally stark story. North American data center colocation vacancy has fallen to a record low of 1%, with 92% of all capacity currently under construction already precommitted before a single cabinet is installed. Enterprises that once planned infrastructure six to twelve months ahead are now securing capacity eighteen to twenty-four months before deployment. Colocation data center providers that cannot deliver power certainty and high-density readiness are being bypassed, not because they are unreliable, but because they are insufficient. The facilities that can deliver are being treated as premium assets, commanding pricing power that reflects their scarcity.

North American Colocation Market Data (2026)

What Does It Actually Take to Make a Colocation Facility AI-Ready?

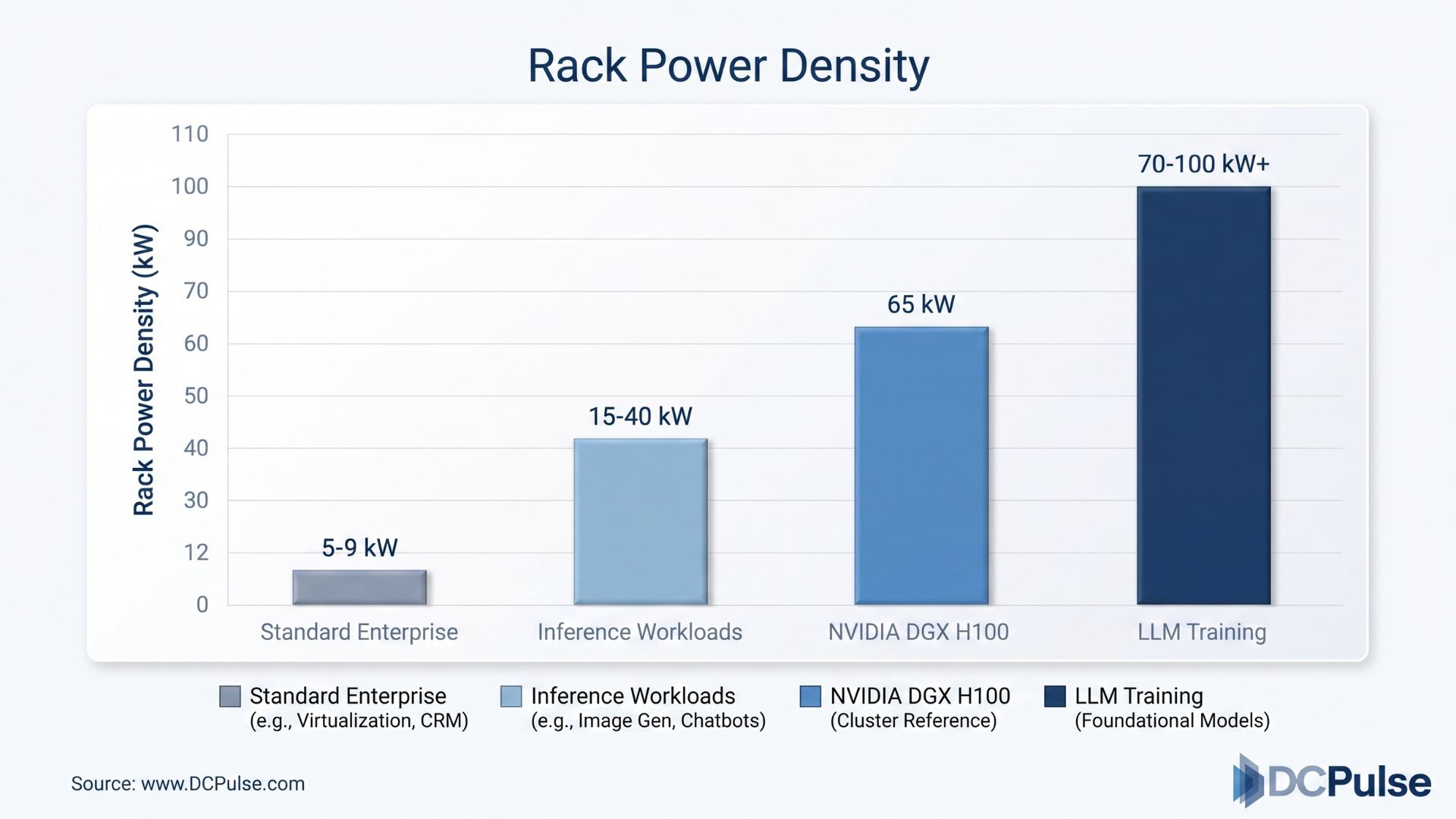

Not every colocation data center can handle AI. The most common rack density across the industry still sits at just 5 to 9 kW per rack, a figure that has barely moved in five years, according to Uptime Institute's Global Data Center Survey 2025. That baseline is sufficient for traditional enterprise workloads. It is entirely insufficient for high-density workloads driven by GPU clusters. The gap between what most facilities offer and what GPU colocation actually requires has created a new category of innovation and a new tier of premium data center colocation services.

The innovations separating a genuinely AI-ready data center solution from a conventional one include:

- High-density power delivery- true AI colocation requires 40 kW per rack as a minimum for inference workloads and 100 kW or higher for large-scale training deployments, with fully redundant power delivery systems at every level.

- Liquid cooling as standard- direct-to-chip cooling, rear-door heat exchangers, and immersion cooling are no longer optional; high-density colocation datacenter operators are deploying liquid-ready infrastructure from day one, with advanced cooling technology penetration reaching 32% across high-density environments.

- Modular and prefabricated construction- factory-integrated, pre-tested infrastructure solutions are cutting deployment times by up to 50% compared to traditional approaches.

- NVIDIA DGX-ready certification- NVIDIA's colocation partner program validates facilities specifically engineered to support DGX infrastructure, creating a verifiable benchmark for AI-ready data center capability.

- Low-latency GPU-to-GPU networking- AI training workloads require network architectures optimised for distributed GPU communication, with InfiniBand and RoCE fabric replacing traditional Ethernet in high-performance clusters

Data Center Rack Density Requirements by Workload Type

Colocation pricing reflects this divide clearly. Data center colocation pricing for 250 to 500 kW deployments reached USD 184 per kilowatt per month in H1 2025, with requirements above 10 MW seeing increases of up to 19% in the same period.

Which Companies Are Betting Biggest on AI-Ready Colocation, and How?

The capital flowing into high-density colocation data center infrastructure in 2025 and 2026 is not incremental. It is transformational, and the deals being struck are redefining who the leading data center colocation companies are and where the next generation of capacity is being built.

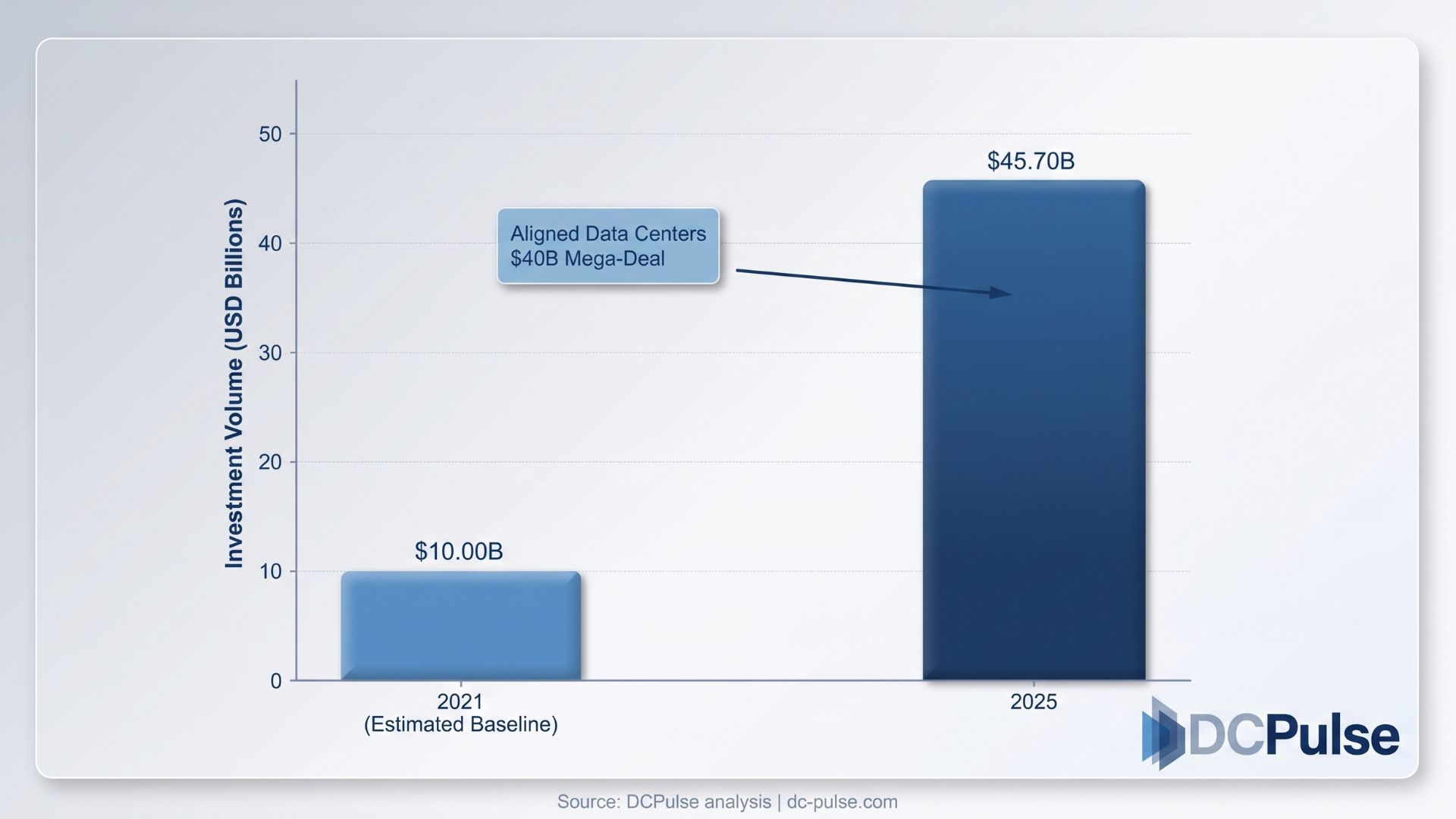

The single most significant signal came from private equity. Private equity investment in U.S. data centers reached USD 45.70 billion in 2025, the highest total in at least five years, with 72% of overall investment in the sector backed by private equity. The defining deal was the planned USD 40 billion acquisition of Aligned Data Centers by a consortium including MGX Fund Management, Microsoft, NVIDIA, BlackRock, and Temasek Holdings. That one transaction reshaped the data center colocation providers' landscape overnight.

US Data Center Private Equity Investment (2021 vs. 2025)

Google and Blackstone moved in the same direction with a joint venture announced in January 2025, creating a new AI-focused company backed by USD 5 billion in Blackstone equity capital, targeting 500 MW of high-density colocation capacity online by 2027. Meanwhile, Cologix committed to an AI-ready 800 MW campus in central Ohio, one of several colocation data center news stories from 2025 signaling that secondary markets are capturing the next wave of supply as Northern Virginia and other primary hubs hit capacity constraints.

The geography of high-density colocation data center development is also shifting. Enterprises searching for a colocation data center near me are increasingly finding that the nearest available AI-ready capacity is no longer in the obvious markets. Ohio, Texas, Louisiana, Nebraska, and Iowa are winning new supply as power availability, not prestige, becomes the primary selection criterion.

What Does the Rise of AI-Ready Colocation Mean for the Decade Ahead?

The global data center colocation market is projected to grow from USD 94.7 billion in 2025 to USD 231.3 billion by 2032, and colocation leads all infrastructure segments in growth rate at 19% CAGR globally, according to JLL's 2026 Global Data Center Market Outlook. The trajectory is clear. But the more important signal is structural; colocation is not just growing, it is bifurcating into two distinct tiers: facilities that can support AI and those that cannot.

For enterprises, the strategic decision has already arrived. Waiting for the right AI-ready facility to become available in your preferred market is no longer a viable plan; 92% of capacity under construction is already precommitted. The organizations securing capacity now, on terms that give them density, power, and scalability, are locking in competitive advantages that will compound over the years.

The colocation facility was once a commodity. The AI-ready version of it is anything but. And the gap between the two is widening faster than most of the market has yet to realize.