A GPU running an AI training job generates heat that air simply cannot move fast enough. Inside a modern hyperscale data center, a single rack of NVIDIA Blackwell GPUs pushes 163 kilowatts of heat, the equivalent of running 1,600 hair dryers simultaneously in a space the size of a wardrobe.

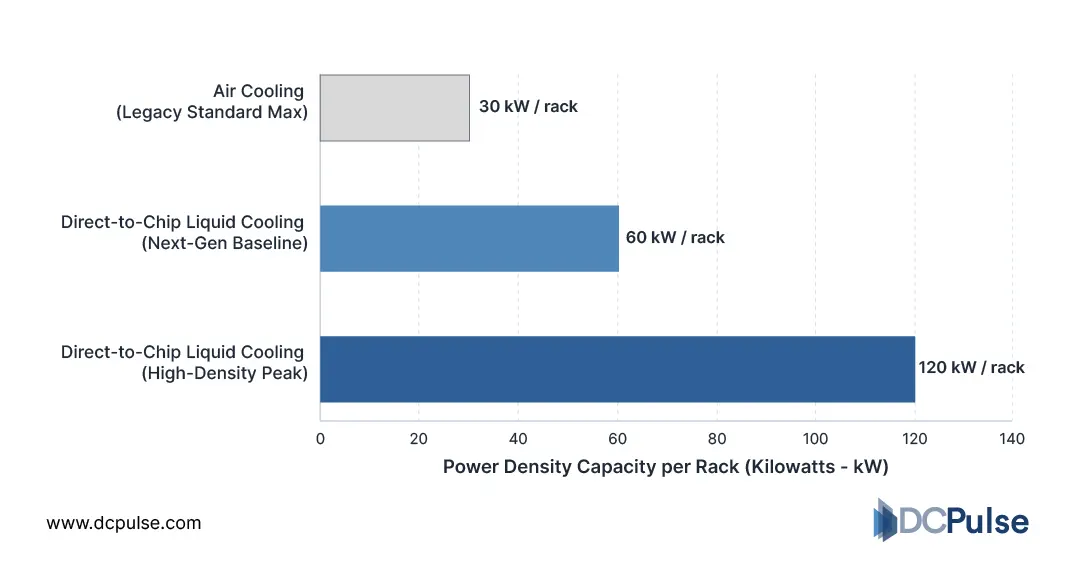

Traditional air cooling, designed for a different era, tops out at around 30 kW per rack. The gap between what AI demands and what air can handle is no longer a future problem. It is a present one.

The answer the industry has landed on is direct-to-chip cooling, and it is quickly becoming the defining infrastructure choice of the AI data center era.

Where Does the Data Center Cooling Market Actually Stand Today?

For most of the last decade, air cooling was the default, cheap to deploy, easy to maintain, and sufficient for the workloads it was asked to handle. That era is closing. What looked ambitious in 2023 is now the desired specification for supporting AI workloads in 2025 and will become the minimum specification for even denser GPU servers in 2026. The industry hasn't gradually drifted toward liquid cooling. It has been pushed there by physics.

Understanding how direct-to-chip cooling works starts with the problem it solves. Direct-to-chip cooling delivers coolant directly to the most thermally demanding components in a server, CPUs, GPUs, and AI accelerators, via cold plates mounted on the chips themselves.

Heat is removed at the source before it can radiate into the surrounding air. By removing 70-80% of heat loads directly at the chip, direct-to-plate cooling reduces the burden on facility-level cooling infrastructure, delivering real-world energy savings of 20-30% and improving PUE from 1.5-2.0 down to significantly lower levels.

Rack density supported: air cooling vs. direct-to-chip cooling (2026)

The market is responding to that performance gap in real time. Direct-to-chip systems already hold the largest share of the liquid cooling market at 42.85% of 2025 revenue. Direct-to-chip and immersion cooling solutions now represent over 38% of all new high-density deployments. Among data center liquid cooling companies, adoption is accelerating fastest in hyperscale environments. Microsoft's Azure AI clusters, Google's TPU deployments, and Meta's LLaMA training nodes have all shifted to liquid cooling.

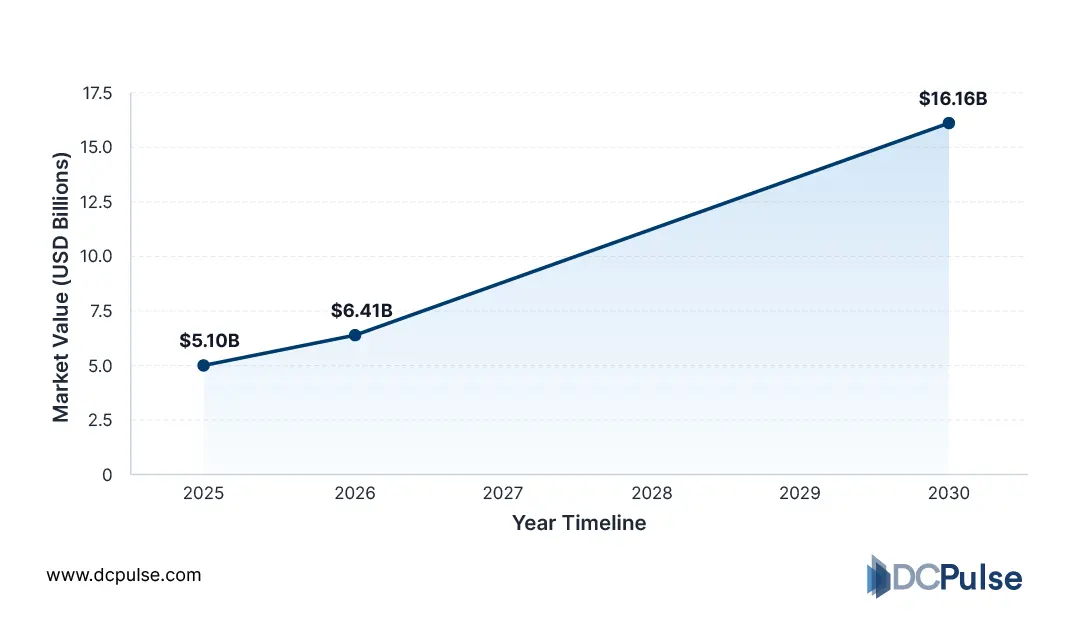

Data center liquid cooling market size growth

What Are the Most Important Innovations Reshaping Data Center Cooling Right Now?

The cooling technology stack is not standing still. As GPU thermal design power increases and rack densities surpass what single-phase systems can handle, the next generation of direct-to-chip cooling companies and engineers are developing solutions that extend far beyond the cold plate.

Two parallel innovation tracks are emerging: one refines direct-to-plate cooling at the chip level, and the other moves toward full liquid immersion.

The most significant innovations reshaping the space include:

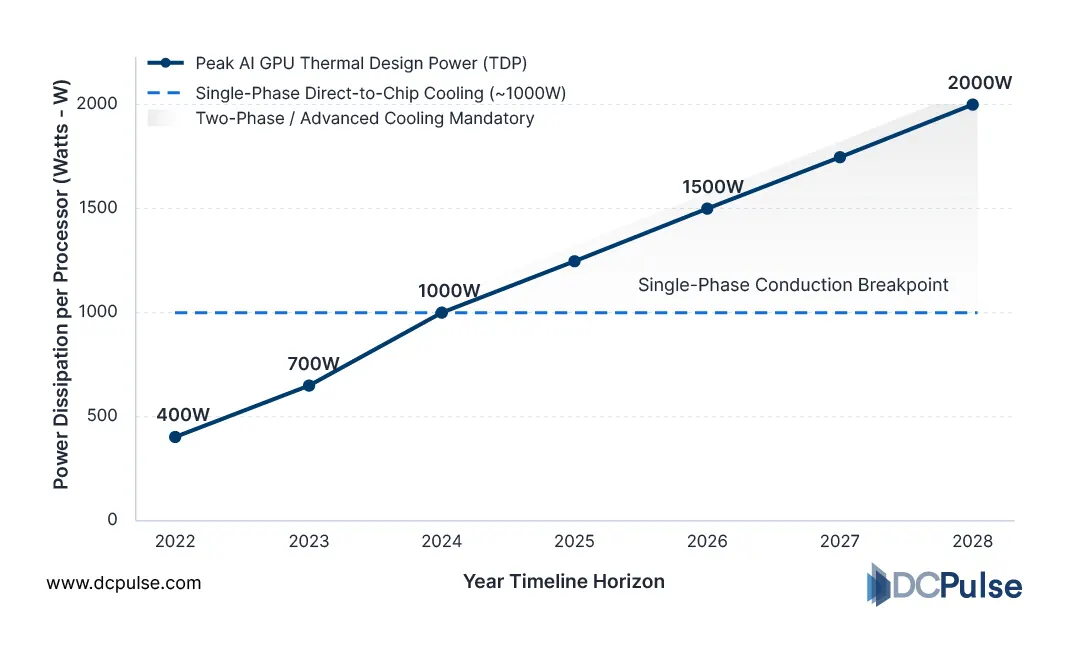

Two-phase direct-to-chip cooling - as of 2025, single-phase D2C cooling remains dominant, but two-phase systems are expected to become essential with large-scale adoption projected for 2026-2027, offering higher heat-transfer coefficients that single-phase cold plates cannot match at extreme TDPs.

Microfluidic cold plates - have channels etched at the microscale directly into chip packaging, removing heat closer to the transistor layer than any previous approach; Microsoft's microfluidic cooling channels promise threefold improvements over traditional cold plates.

ZutaCore waterless two-phase direct-on-chip cooling - a partnership with Valeo advancing a waterless system aimed at improving efficiency and sustainability without the risks of water leakage in high-density environments.

Waste heat recovery integration - directing captured heat into district heating networks or on-site energy reuse systems, turning a cost center into a sustainability asset

AI-driven cooling controls - intelligent monitoring systems that dynamically adjust coolant flow rates and temperatures in real time based on workload demands, reducing energy waste without compromising thermal performance

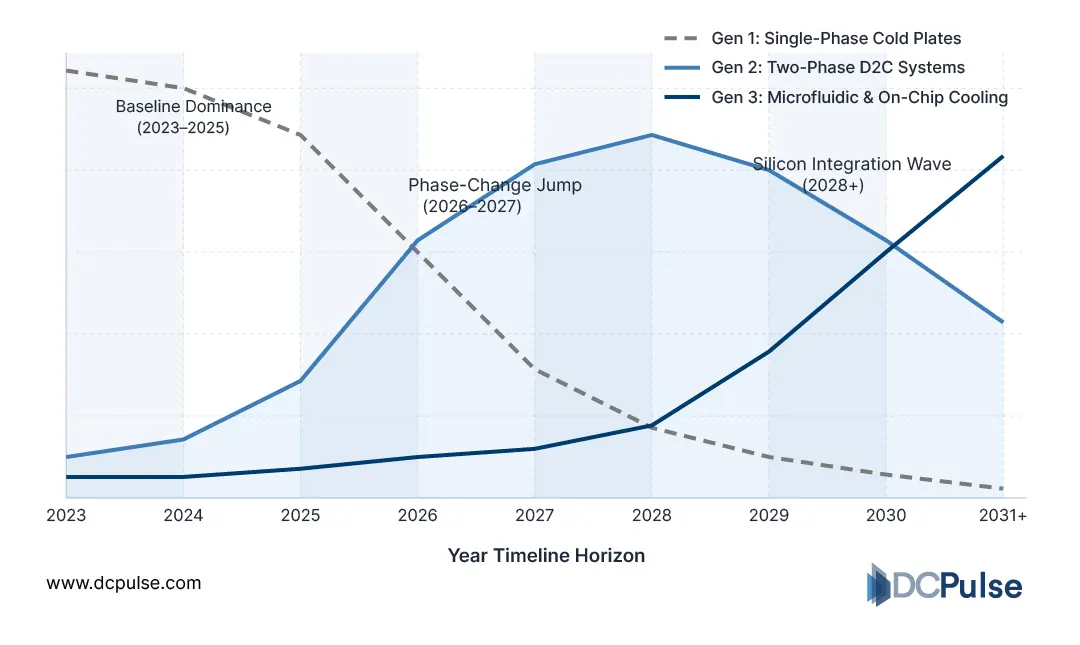

Direct-to-chip cooling evolution

IDTechEx projects that future GPUs will push well beyond the limits of single-phase cooling, making the transition to two-phase and advanced direct-to-plate cooling not a choice but an engineering inevitability.

GPU Thermal Design Power (TDP) vs. Single-Phase Liquid Cooling Limits (2022–2028)

Which Companies Are Shaping the Future of Direct-to-Chip Cooling?

The cooling industry is consolidating fast, and the acquisitions and product launches of the last twelve months make it clear that direct-to-chip cooling is no longer a niche. It is becoming the backbone of AI data center infrastructure, and the companies that own that stack are becoming strategically valuable.

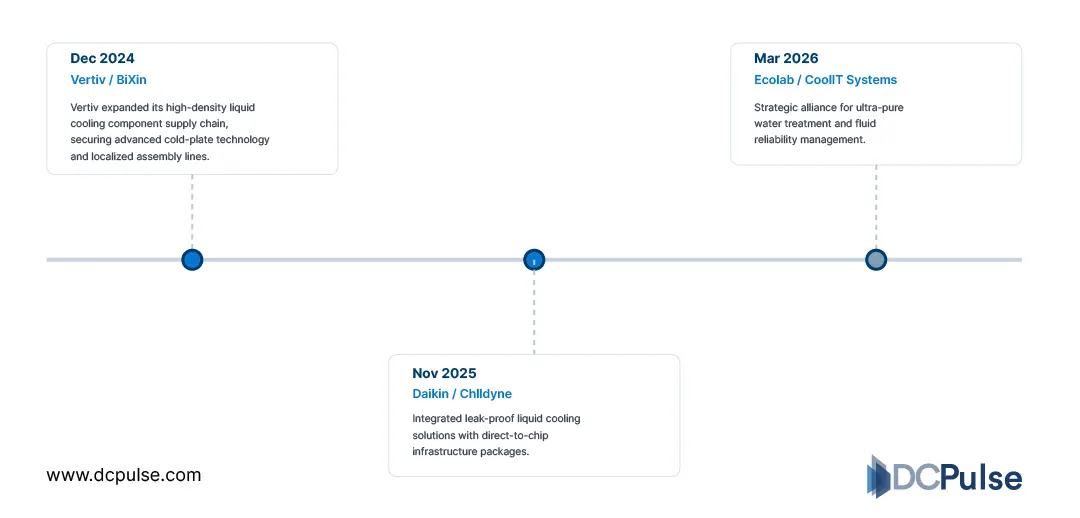

The most significant move came in March 2026. Ecolab announced a definitive agreement to acquire CoolIT Systems, a pure-play data center liquid cooling company designing and manufacturing CDUs, cold plates, and direct-to-chip cooling technologies, from funds managed by KKR. CoolIT counts NVIDIA and AMD among its custom engineering clients. The deal positions Ecolab as a full-stack cooling solutions provider almost overnight.

Daikin Applied made a parallel move in November 2025, acquiring Chilldyne to expand its data center cooling portfolio with direct-to-chip liquid cooling technology.

Key direct-to-chip cooling M&A activity

On the product side, Accelsius launched the NeuCool IR150 at Data Center World 2026, the industry's first fully integrated rack-level two-phase cooling solution combining a CDU, 42U of IT rack space, and built-in liquid and vapor manifolds in a single enclosure, offering up to 150 kW of capacity. The system is designed to bring two-phase direct-to-plate cooling within reach of enterprises, not just hyperscalers. By 2026, direct-to-chip liquid cooling is widely considered the industry standard for state-of-the-art AI data center facilities.

What Does the Road Ahead Look Like for Data Center Cooling?

The trajectory is set. The global direct-to-chip cooling market is projected to grow from USD 3.33 billion in 2026 to USD 17.31 billion by 2032, at a CAGR of 26.5%. Rising rack densities above 30 kW, accelerating GPU deployments for AI workloads, and tightening sustainability mandates are converging to make liquid cooling a core architectural requirement for modern facilities. This is no longer a premium option. It is becoming the baseline.

For data center operators, the strategic implication is straightforward: facilities designed around air cooling are already approaching obsolescence for high-density AI workloads. The question is no longer whether to transition; it is how fast and which cooling architecture fits the workload mix.

For the broader industry, direct-to-chip cooling marks a fundamental shift in how data centers are engineered, from the outside in, cooling the building, to the inside out, cooling the chip. The heat problem isn't going away. The infrastructure is finally catching up to it.