The customer taps their card.

The terminal beeps.

And for a fraction of a second, nothing happens.

In that pause lives an entire financial decision.

The bank has to verify the account, the network has to route the request, a risk engine has to score fraud probability, and a response has to come back before the shopper pulls the card away. The system is expected to feel instantaneous, yet behind the screen a chain of institutions briefly negotiates trust.

For decades, payments were designed around tolerance for delay. Authorisation could travel across regions, fraud models could take their time, and settlement would happen hours later anyway. Speed was convenience, not correctness.

That assumption no longer holds.

Real-time payment rails, contactless expectations, and digital commerce have compressed decision windows to the point where distance itself becomes part of the risk model. A transaction delayed too long is treated the same as a suspicious one: it fails. Not because the account lacks funds, but because the system cannot decide fast enough.

In modern payment systems, latency is no longer a performance metric.

It is part of the approval logic.

And the place where that decision is computed, sometimes just a few kilometres closer to the card reader, increasingly determines whether money moves or the moment breaks.

When “Instant” Became Mandatory

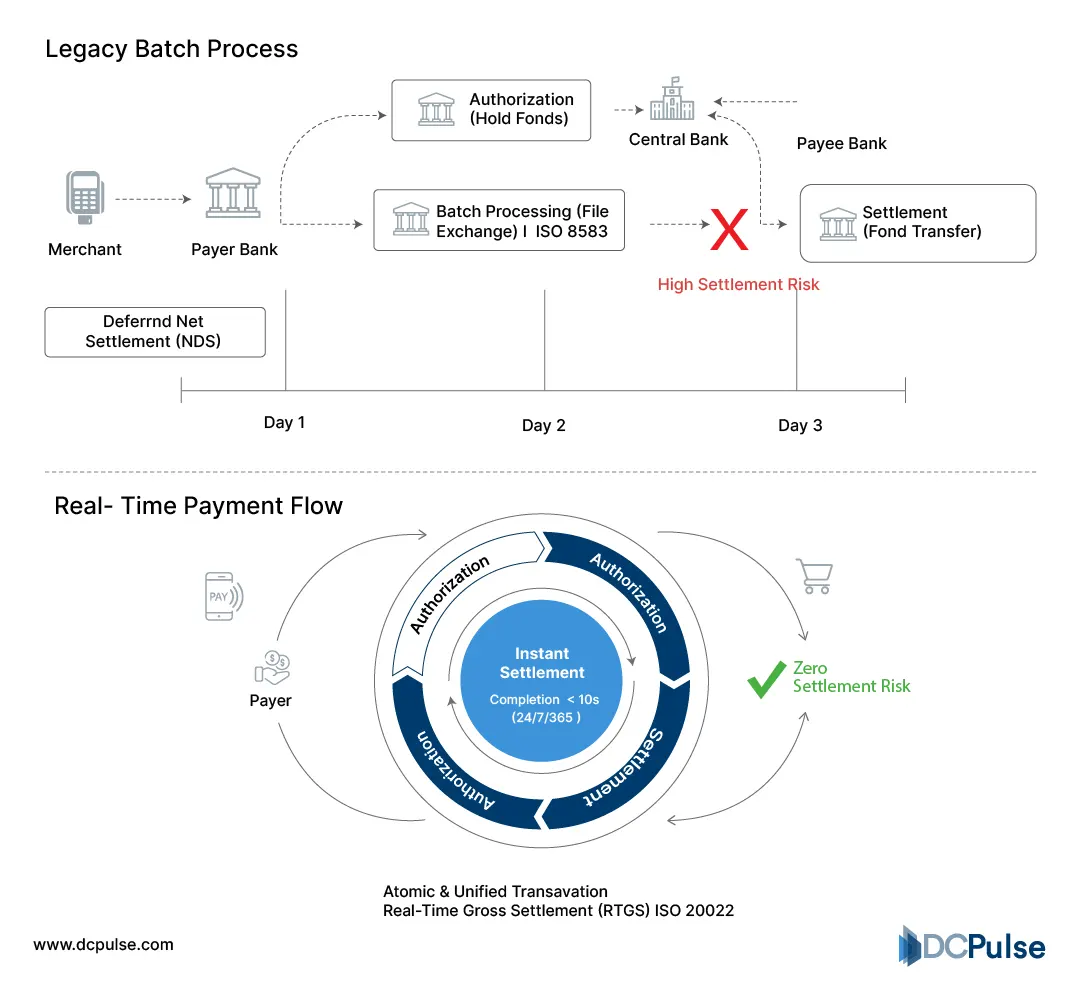

For most of modern banking history, authorisation and money movement were separate events. A card approval meant the bank intended to pay; settlement confirmed it later. The delay gave networks tolerance for distance; a transaction could travel across countries and still succeed because time was built into the system.

That architecture changed once payment rails began guaranteeing immediacy.

India’s UPI requires near-real-time confirmation and operates continuously, processing billions of transactions monthly under strict response expectations. The U.S. FedNow Service requires participating institutions to respond to payment messages within defined time limits for instant transfers. SEPA Instant mandates fund delivery within seconds across Europe.

In practice, this collapses the historical gap between authorisation and settlement. The approval is no longer provisional; it becomes the financial event itself.

Legacy vs Real-Time Payment Flow

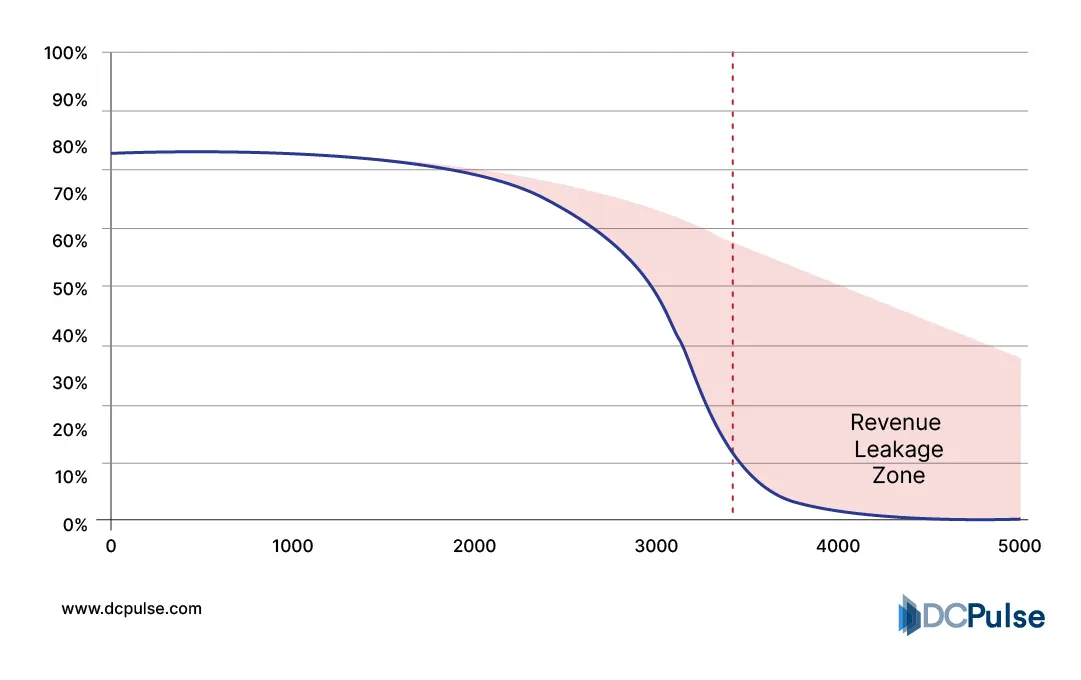

This compression introduces a new constraint: decision time must fit human behaviour. Checkout systems cancel requests if responses exceed operational thresholds, and payment gateways retry automatically when acknowledgements are delayed. The consequence is not just slower service; it is higher failure probability.

Payment networks openly track this relationship. Visa’s merchant performance guidance shows authorisation rates decline as response latency increases beyond expected ranges. So, speed has become part of correctness.

At the same moment, risk evaluation expanded. Modern approvals can include behavioural signals, device recognition, token verification, and transaction history checks before issuing a response.

The system must therefore make a more complex decision in a smaller window.

Geography now matters financially. When authorisation must travel long distances to reach a centralised risk engine and return, delay consumes the available decision window. A legitimate payment can fail simply because the confidence calculation arrives too late.

The industry increasingly measures reliability not as uptime, but as approval certainty within a fixed time boundary.

Approval Probability vs Time Threshold

In modern payment systems, the difference between accepted and declined is often not fraud, funds, or identity, but whether the system decided fast enough.

Approval Reliability Now Depends on Where the Decision Happens

Real-time payments forced the industry to confront a physical constraint: a transaction cannot wait longer than the customer does.

Instant rails such as FedNow and SEPA Instant require participating institutions to respond to payment messages within strict operational time limits, meaning the approval must arrive while the interaction is still in progress. The approval is no longer a preliminary signal; it is the payment outcome.

That changed the question from how to compute a decision to where the decision should be computed.

Historically, authorisation logic sat deep inside centralised banking systems. The transaction travelled to the bank, the bank evaluated risk, and a response returned. But when response time determines whether a payment succeeds, distance begins acting like uncertainty. Even a legitimate transaction can fail if confidence arrives too late.

Payment networks therefore shifted evaluation outward, positioning decision logic along the transaction path instead of only at its destination.

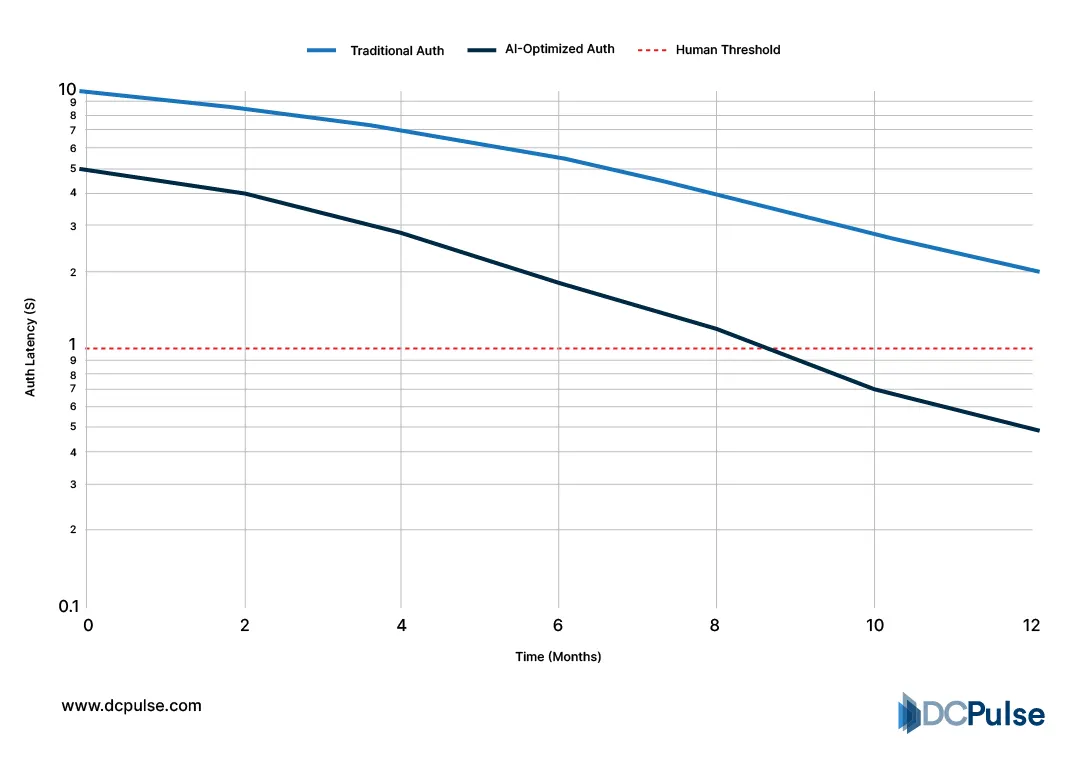

Authorization Latency vs. Human Interaction (0-12 Months)

Security controls moved as well. In instant payment environments, fraud mitigation must occur before settlement rather than after investigation, requiring real-time inline risk scoring during authorisation.

Because of that, systems rely on immediately available signals, recent activity familiarity, token validity, and behavioural patterns instead of reconstructing full account history from a distant core system. The goal is confident certainty within the response window, not perfect certainty outside it.

Card network performance guidance shows authorisation success rates decline as response latency increases, reinforcing why predictable timing matters as much as correctness.

To maintain reliability, modern payment architectures distribute validation steps across regional processing locations. The transaction receives an initial confidence decision nearby, then final confirmation afterward.

This creates a reversal in payment design philosophy; transactions no longer travel to a single place of truth; truth forms near the transaction and is reconciled afterward.

In modern payments, approval depends less on computational power and more on decision proximity.

How the Industry Is Repositioning Payment Infrastructure

Payment reliability is increasingly determined before the issuer ever responds.

Card networks operate distributed authorisation processing so transactions can be evaluated within predictable response windows regardless of where the card is used. Real-time authorisation messaging is handled across multiple network locations rather than a single central processor.

The goal is not speed alone; it is consistency. A card should be approved in a similar time whether used locally or internationally.

Instant payment systems reinforced the same behaviour. Real-time infrastructures require participating institutions to process and respond within strict time limits, which effectively forces processing to occur near the transaction origin.

Instead of accelerating long paths, the industry shortened them.

Regulation then aligned with performance. Data localisation and domestic processing rules mean certain payment validations must occur within national infrastructure boundaries, naturally reducing authorisation travel distance.

Cloud regional computing environments allow payment platforms to place transaction logic near users while keeping core banking centralised.

The Next Competitive Layer in Payments

Payments are no longer judged only by security or speed but by whether a decision arrives within the moment of interaction. Real-time rails removed the buffer that once separated authorisation from completion. Now the system must be confident fast enough for the purchase to continue.

This changes how institutions think about risk. Instead of waiting for perfect certainty, they increasingly act on immediate confidence and resolve ambiguity afterward. The first answer enables the transaction; later processes protect the balance sheet. Reliability therefore becomes a timing discipline as much as a financial one.

For merchants and consumers, this shift appears simple: the payment either works or it does not. But underneath, the industry is reorganising around decision placement rather than processing scale. Approval stability becomes a competitive feature.

The strategic implication is clear. Payments are evolving into interaction systems, where trust must exist at the exact moment of exchange. Systems that decide nearby and confirm later will outperform systems that decide perfectly but arrive late.

The future of payments will be defined by proximity of judgement.