For years, data center expansion followed a familiar logic: build where power is cheap, land is available, and demand is predictable. That logic is breaking down in emerging markets. Today’s growth regions, across Asia, Africa, Latin America, and parts of the Middle East, offer enormous digital upside. Still, they also expose operators to infrastructure fragility, regulatory uncertainty, and geopolitical risk that mature markets rarely present.

Demand for cloud services, digital payments, AI inference, and streaming is accelerating in these regions, often outpacing the readiness of local grids, networks, and permitting frameworks. In response, data center footprints are no longer just capacity decisions; they have become strategic choices about resilience, control, and long-term exposure. Where facilities are built, how large they are, and how quickly they can adapt now shape competitive advantage as much as cost efficiency.

As operators reassess expansion strategies, the question is no longer whether emerging markets matter; they clearly do, but the question is whether traditional hyperscale models are suited to the realities on the ground. Rethinking data center footprints has become a board-level imperative.

The Reality of Building in Emerging Markets

In emerging markets, data center demand is rising faster than the infrastructure meant to support it. Cloud adoption, digital public services, fintech, and mobile-first consumption are expanding rapidly, yet power grids, fiber networks, and permitting systems often lag behind. For executives, this creates a structural mismatch: markets with strong demand signals but uneven operating foundations.

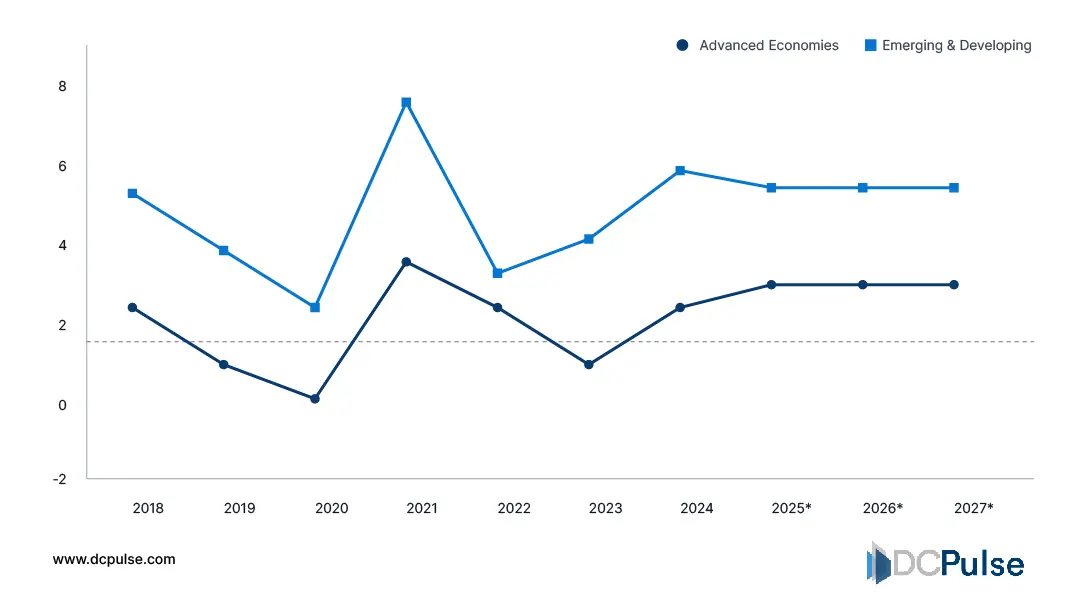

Power remains the defining constraint. In many high-growth regions, grid reliability varies by geography and season, forcing operators to plan for on-site generation, energy storage, or long-term power purchase agreements earlier than they would in mature markets. The International Energy Agency notes that electricity demand in emerging and developing economies is growing at more than twice the pace of advanced economies, intensifying competition for stable capacity.

Annual Electricity Demand Growth (%)

Regulatory complexity adds another layer. Data localization rules, foreign ownership limits, and inconsistent permitting timelines can materially affect site selection and time-to-market. The World Bank has highlighted how regulatory uncertainty remains a key deterrent to large-scale digital infrastructure investment in developing economies.

Finally, network proximity matters. As mobile broadband and real-time applications scale, latency sensitivity increases, pushing compute closer to users. GSMA data shows that over 90% of new mobile subscribers through 2030 will come from emerging markets, reinforcing the need for geographically distributed capacity.

Together, these factors force a rethink: footprint strategy in emerging markets is no longer about size alone but about flexibility, risk management, and alignment with local realities.

New Footprint Strategies Are Replacing the Hyperscale Playbook

As emerging markets mature digitally, operators are rethinking how capacity is deployed, not just where. The most significant innovation is not a new technology stack but a shift in footprint strategy itself.

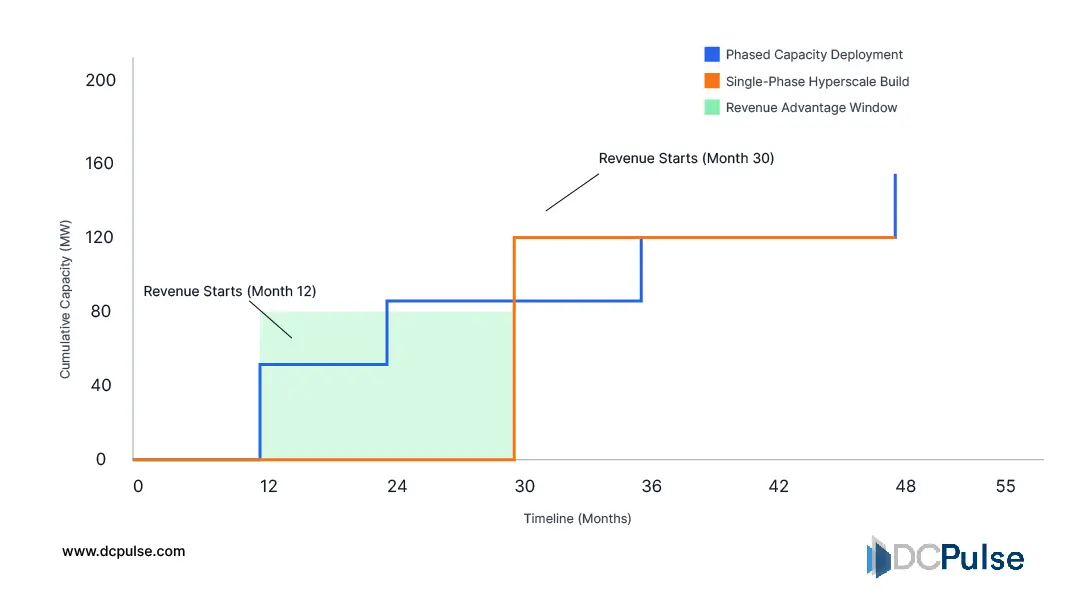

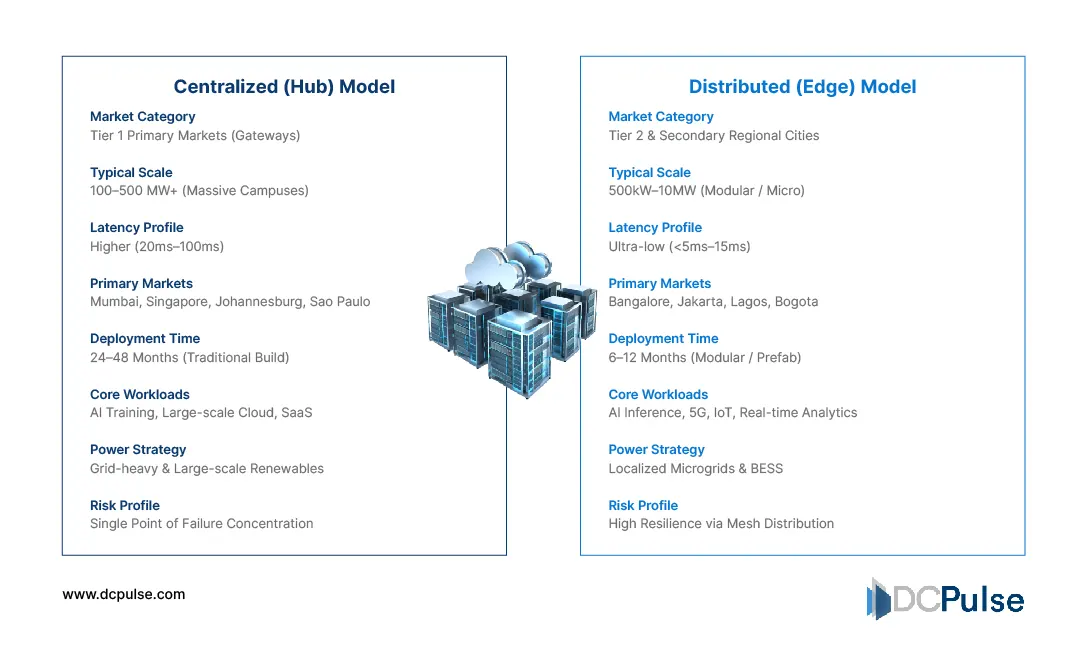

One clear trend is the move toward modular and phased development. Rather than committing billions upfront to hyperscale campuses, operators increasingly deploy capacity in stages, aligning capital expenditure with demand certainty and regulatory clarity. The phased expansion reduces exposure to power delays, permitting risks, and demand forecasting errors, issues that are far more pronounced in emerging economies.

Phased Deployment vs. Single-Phase Hyperscale Build

Energy strategy is also being redesigned. In many emerging markets, grid instability and long interconnection timelines are forcing operators to plan for partial energy autonomy from day one. The International Energy Agency highlights that reliability constraints and demand growth in developing economies are accelerating interest in on-site generation, storage, and long-term renewable PPAs as part of infrastructure planning, not as retrofits.

A third shift is toward distributed regional footprints. Instead of concentrating capacity in a single mega-campus, operators are placing smaller facilities closer to population centers to manage latency, improve resilience, and comply with data localization rules. The World Bank has identified data sovereignty and regulatory fragmentation as key drivers pushing digital infrastructure toward more localized deployment models in emerging markets (World Bank – Digital Infrastructure).

Centralized Hubs vs. Distributed (Edge) Deployment

Together, these shifts signal a fundamental change: success in emerging markets depends less on raw scale and more on flexibility, risk management, and strategic sequencing.

How Cloud Providers and Operators Are Shaping Footprints in Emerging Markets

As emerging markets evolve into priority growth regions, major infrastructure players are adjusting footprint strategies to balance opportunity with operational risk. One of the most visible trends is the expansion of hyperscale and colocation infrastructure into Latin America, Southeast Asia, and Africa to align capacity with cloud adoption, AI workloads, and regulatory requirements.

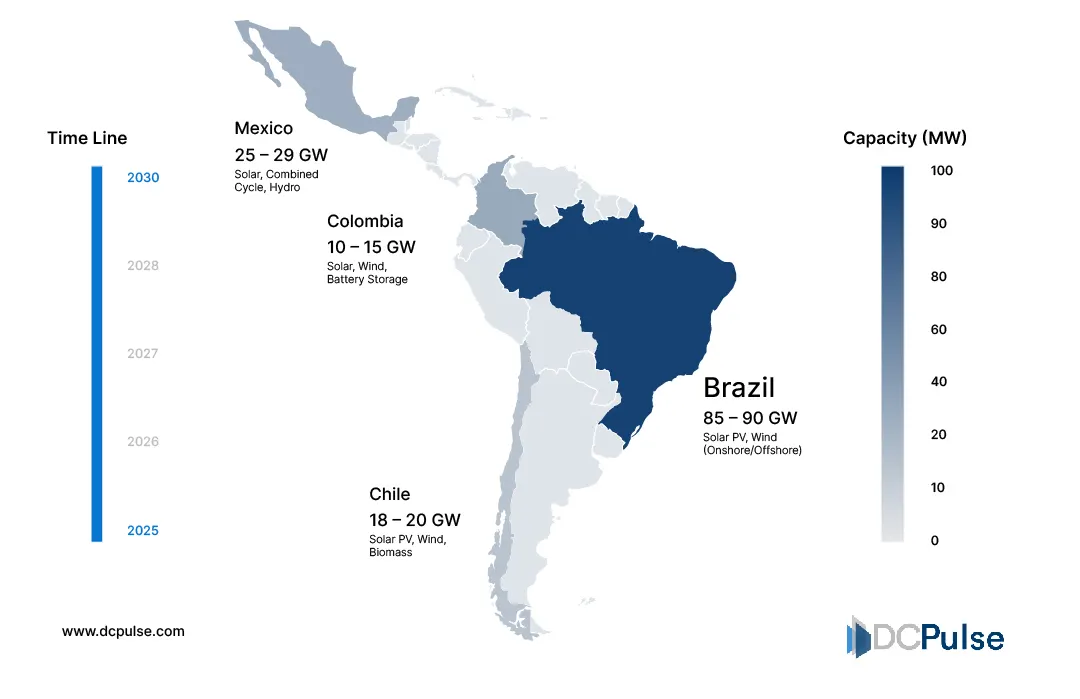

In Latin America, data center investment is accelerating sharply. Market forecasts project that operators will add more than 1,800 MW of capacity between 2025 and 2030, with Brazil leading global colocation growth due to strong cloud and enterprise demand. This expansion reflects a deliberate shift toward regional capacity hubs rather than reliance on intercontinental links alone.

Projected Data Center Capacity Additions (2025–2030)

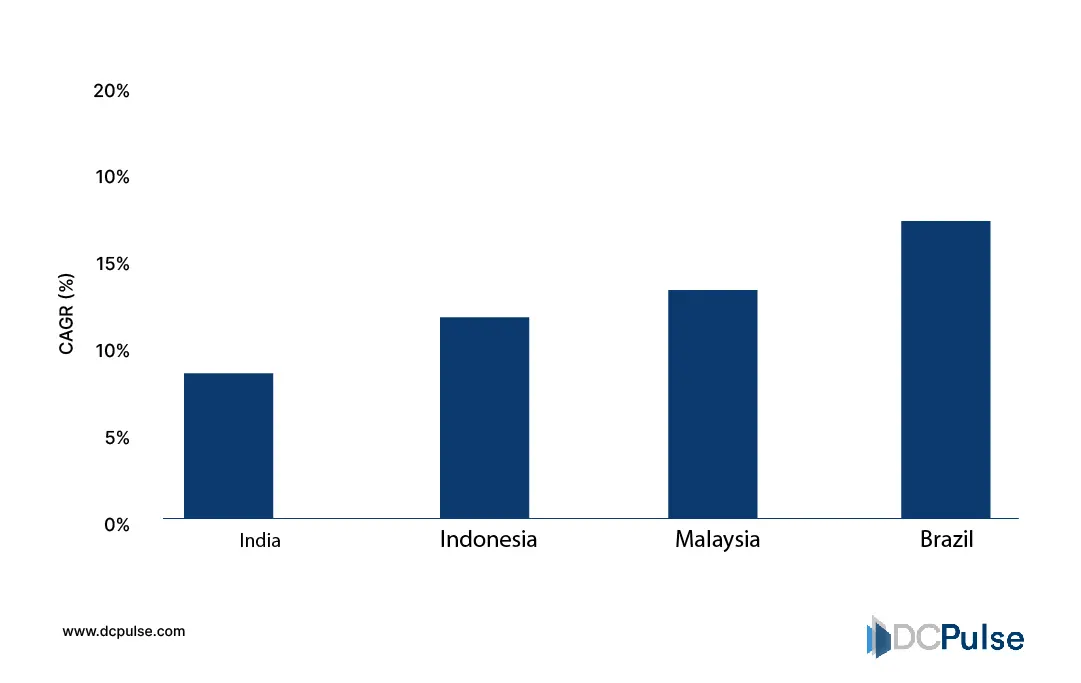

Emerging Asian markets are also attracting major builds. India’s installed base is set to grow rapidly, with government policies like data localization and digitalization incentives drawing hyperscale cloud investments to Mumbai, Hyderabad, and Bangalore. Southeast Asia, especially Malaysia and Indonesia, has seen rising interest from global players due to cost advantages and expanding connectivity infrastructure.

Data Center CAGR Comparison - India, Malaysia, Brazil and Indonesia - (2025–2030)

Africa’s data center landscape is similarly transforming. Regional operators like Africa Data Centers and global entrants such as Equinix and Digital Realty are expanding colocation and wholesale capacity to support cloud growth and local digital ecosystems. Governments and development institutions are co-investing, underlining the strategic importance of local infrastructure autonomy.

These moves illustrate a broader industry strategy: rather than cloning mature-market footprints, operators are tailoring configurations, partner ecosystems, and growth pacing to match emerging-market realities. Footprint decisions are increasingly driven by local demand curves, energy constraints, regulatory landscapes, and connectivity opportunities, rather than by one-size-fits-all expansion models.

Footprint Strategy Becomes a Competitive Advantage

As emerging markets move from peripheral growth zones to core digital economies, data center footprints are becoming a defining strategic choice. The era of copying mature-market hyperscale models is fading. Instead, operators must design footprints that reflect uneven grid reliability, evolving regulatory frameworks, and uncertain demand curves.

The most resilient strategies prioritize flexibility over sheer scale. Phased deployments, modular expansion, and distributed regional capacity allow operators to manage capital exposure while responding quickly to market signals. Energy planning is equally strategic. In markets where grid constraints persist, early investment in power diversification, through renewables, storage, and long-term PPAs, reduces operational risk and improves long-term cost predictability, as highlighted by the International Energy Agency’s assessment of electricity reliability in developing economies.

Regulation and sovereignty considerations will further shape footprint decisions. The World Bank notes that data localization and national digital strategies increasingly influence where and how infrastructure is deployed.

Ultimately, success in emerging markets will favor operators that treat footprint planning not as a construction exercise but as a long-term strategic capability.