The global data center industry is entering a phase of rapid consolidation, driven not just by organic growth but by an accelerating wave of mergers and acquisitions (M&A). As demand surges across cloud computing, artificial intelligence, and enterprise workloads, building and scaling data center infrastructure has become increasingly capital-intensive, requiring significant investment in land, power, cooling, and connectivity.

In response, operators and investors are turning to M&A as a primary strategy to expand capacity, enter new markets, and secure strategic assets. Investment firms such as Blackstone and Brookfield Asset Management have been actively acquiring and consolidating data center platforms, signaling strong confidence in the sector’s long-term growth trajectory.

At the same time, hyperscale demand is pushing providers to build globally integrated platforms, often through acquisition-led expansion rather than standalone development.

In this environment, M&A is no longer just a growth lever; it is the mechanism through which consolidation is actively reshaping the structure and competitive dynamics of the data center industry.

Scaling Through Acquisition: The New Structure of the Data Center Market

The data center industry is undergoing a sharp increase in mergers and acquisitions (M&A), driven by the need to rapidly scale infrastructure in response to hyperscale and AI demand. A defining example is Blackstone’s acquisition of QTS Realty Trust, one of the largest data center deals in history, valued at approximately USD 10 billion, including debt.

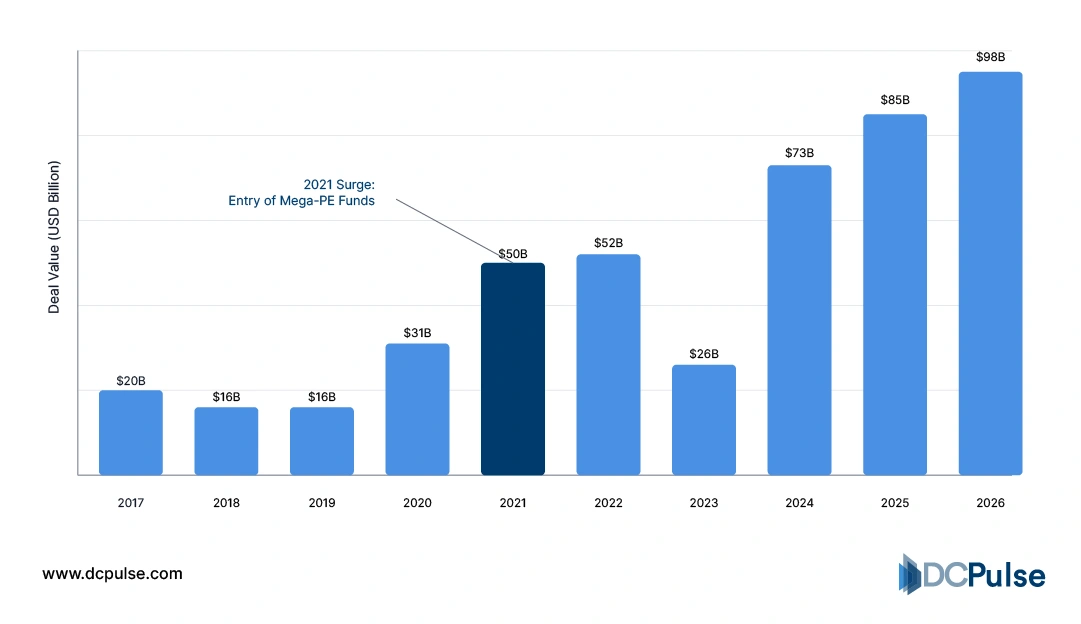

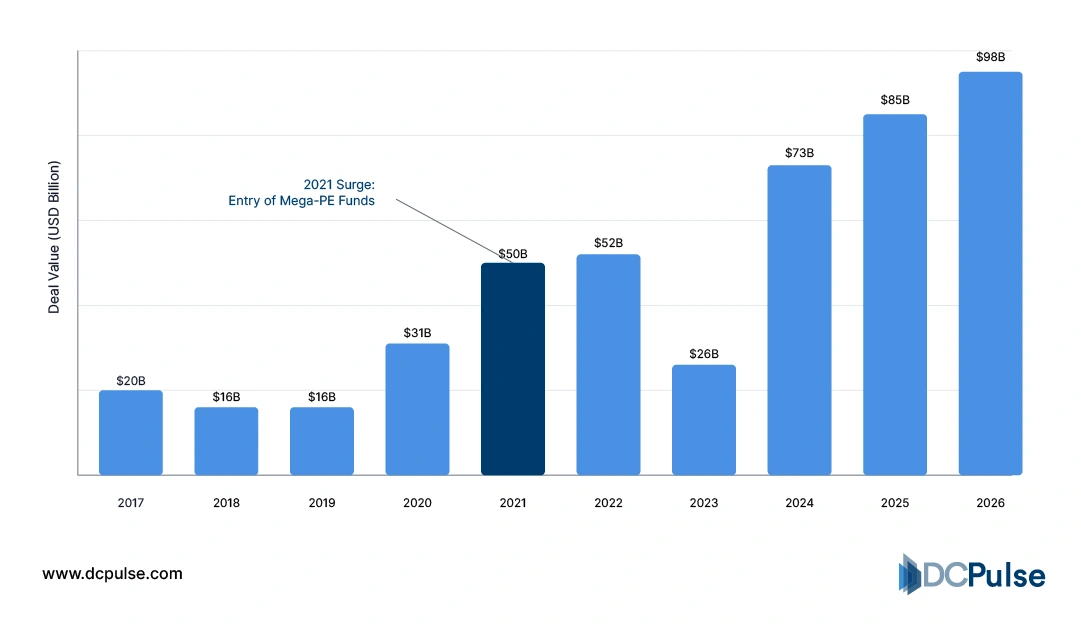

This transaction was not an isolated event but part of a broader surge in deal activity. Industry data shows that data center M&A deals exceeded USD 23 billion in 2021, highlighting the scale at which capital has entered the sector.

Global Data Center M&A Deal Value (2017-2026 Projections)

Institutional investors are playing a central role in this transformation. Firms like Brookfield Asset Management are increasingly targeting digital infrastructure assets, using acquisitions to build globally distributed platforms aligned with long-term demand for cloud and AI workloads.

At the same time, ownership models are evolving into tightly coupled ecosystems, where investor capital, operator platforms, and hyperscale tenants are interdependent. Long-term leasing agreements with cloud providers help de-risk acquisitions and support large-scale financing strategies.

As a result, competitive advantage in the data center industry is increasingly defined by the ability to acquire, integrate, and scale assets across regions, rather than relying solely on organic expansion.

How Are Emerging Technologies Reshaping Post-M&A Integration in the Data Center Industry?

As consolidation accelerates, the real challenge in data center M&A is no longer acquisition; it is integration at scale. Operators must rapidly unify infrastructure, standardize operations, and optimize capacity across geographically distributed assets.

One of the most important enablers is platform-based architecture. Companies like Equinix have built globally distributed platforms centered on interconnection, allowing acquired facilities to be integrated into a unified ecosystem rather than operated as standalone sites. This approach enables consistent service delivery across regions while improving network density and customer reach.

Similarly, Digital Realty has focused on standardizing infrastructure through its global platform strategy, enabling customers to deploy workloads seamlessly across multiple locations. This model is critical in post-M&A environments, where operational consistency determines how quickly assets can be monetized.

Another key innovation is the increasing use of automation and software-defined operations, which allow operators to manage distributed assets through centralized control layers. This reduces integration timelines and improves efficiency across acquired portfolios.

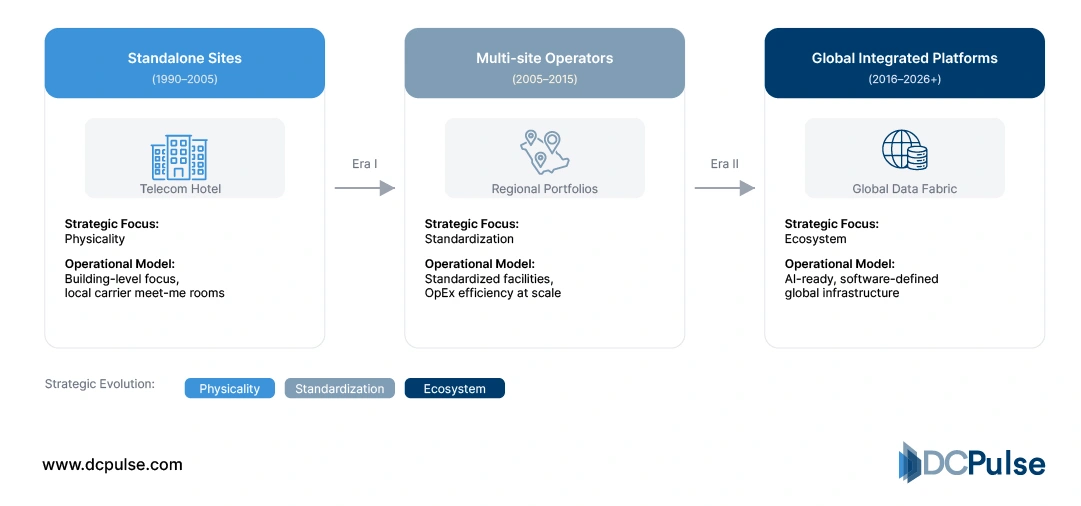

Evolution of Data Center Platforms (1990 – 2026+)

As a result, emerging technologies are shifting M&A from simple expansion to platform-driven consolidation, where success depends on the ability to integrate, standardize, and scale assets into cohesive global infrastructure networks.

Deal-Driven Expansion: The Transactions Reshaping the Data Center Market

The current wave of consolidation in the data center industry is being defined by a series of high-value acquisitions and strategic investments, as operators and investors race to build scale and secure critical infrastructure assets.

One of the most significant moves remains the acquisition of Interxion by Digital Realty, a deal valued at approximately USD 8.4 billion, which expanded Digital Realty’s footprint across key European markets and strengthened its position as a global platform provider.

Similarly, Equinix has pursued acquisition-led growth to expand its global interconnection platform, including multiple regional acquisitions that enhance its presence in high-demand markets and increase network density.

Private equity firms are also playing a decisive role. KKR has been actively investing in digital infrastructure, including data center platforms, as part of a broader strategy to capitalize on long-term demand for cloud and AI-driven workloads.

Top Data Center M&A Deals by Enterprise Value

These transactions illustrate a clear pattern: scale is increasingly being achieved through acquisition rather than organic buildouts. As competition for power, land, and connectivity intensifies, M&A is becoming the primary mechanism through which operators expand geographically and strengthen their market position.

Will Consolidation and M&A Continue to Reshape the Data Center Industry?

Consolidation and M&A are set to remain central to the evolution of the data center industry, driven by the need for scale, capital efficiency, and global reach. As demand from cloud providers and AI workloads continues to surge, operators will increasingly rely on acquisitions to secure power, land, and established infrastructure in key markets where new development is constrained.

However, this trend is not without challenges. Rising asset valuations, limited power availability, and regulatory scrutiny could slow the pace of large-scale transactions. At the same time, integrating acquired assets into unified platforms requires significant operational discipline, particularly as portfolios expand across regions.

Despite these constraints, the long-term direction is clear. The industry is moving toward a model dominated by large, globally integrated platforms, where a small number of operators control extensive, interconnected infrastructure networks.

In this environment, M&A is not just a growth strategy; it is becoming the primary mechanism through which competitive advantage is built, enabling companies to scale faster, enter new markets, and meet the escalating demands of the digital economy.