Data centers like to describe themselves in absolutes

Carbon neutral. Renewable-powered. Net zero on paper.

Yet the reality around them is more complicated. Energy demand is rising faster than grids can adapt, AI workloads run without pause, and the electricity feeding digital infrastructure is still shaped by geography, fuel mix, and timing. In response, the industry has leaned heavily on energy credits and carbon audits, tools designed to translate messy physical systems into clean accounting outcomes.

For years, that translation worked. Today, it is being tested.

As data centers expand into new regions and scale into unprecedented load profiles, the gap between reported sustainability and lived environmental impact is becoming harder to ignore. The question is no longer whether carbon accounting exists, but whether it still reflects how data centers actually operate.

How Carbon Accounting Took Shape in Data Centers?

At the center of most sustainability claims in the data center industry is carbon accounting, a system designed to translate energy use and operational activity into comparable emissions data. Its role is not to explain how power flows through a facility, but to standardise how environmental impact is measured, reported, and audited across regions and operators.

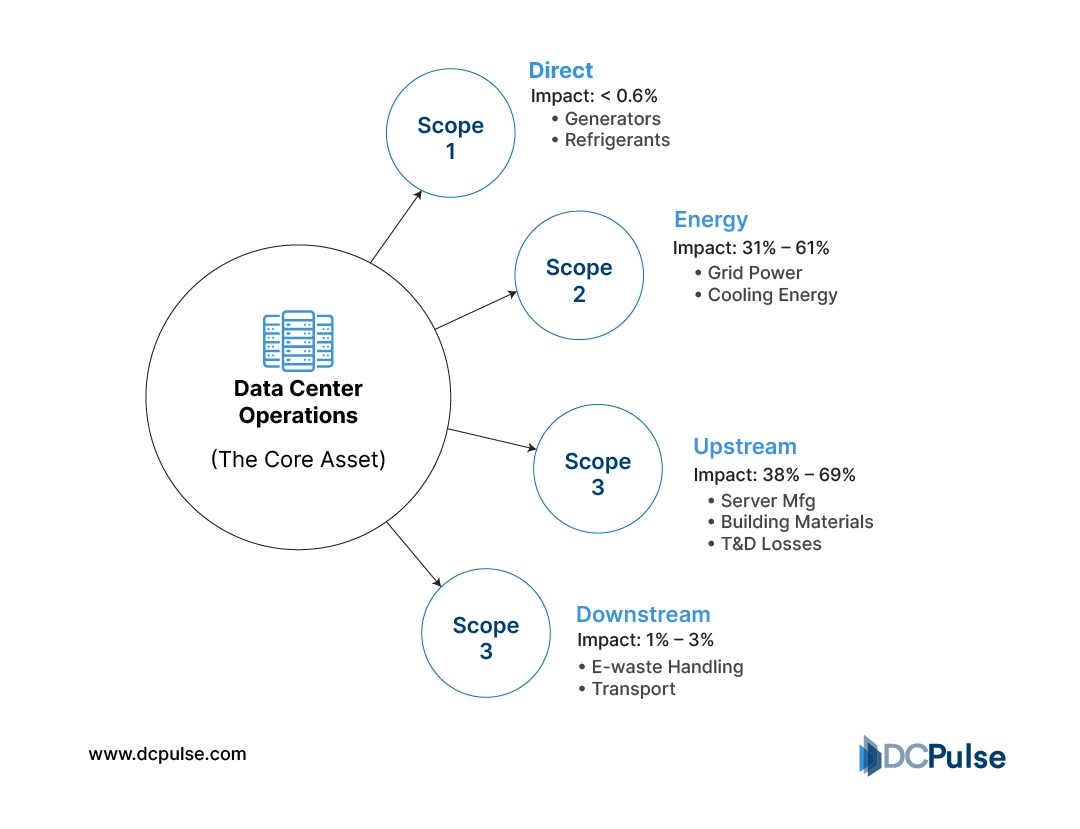

Most data centers follow the Greenhouse Gas Protocol, which organises emissions into three scopes.

Scope 1 covers direct emissions from assets under an operator’s control, such as diesel consumed during generator testing or outages, along with refrigerant leakage from cooling systems. While usually a smaller share of total emissions, these sources are operationally visible and relatively straightforward to track.

Scope-based emissions flow across data center operations

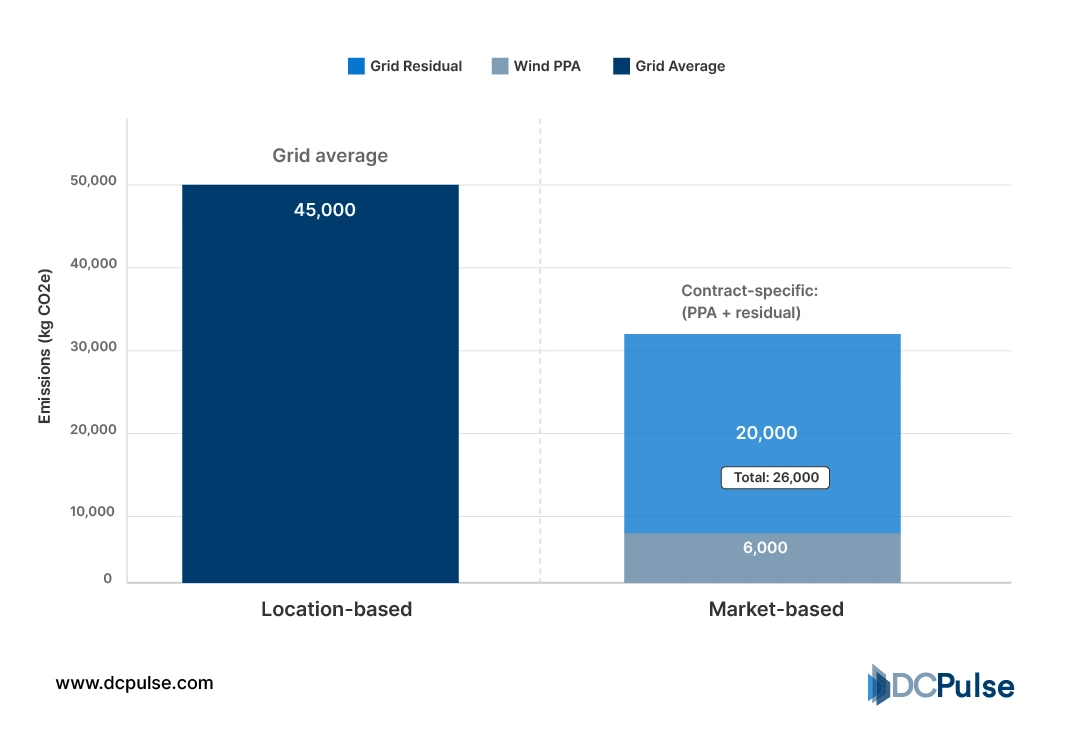

Scope 2 accounts for emissions linked to purchased electricity and dominates the operational footprint of most data centers. Because facilities are highly electrified and operate continuously, grid carbon intensity becomes the primary variable. To manage this exposure, operators rely on market-based instruments such as renewable energy certificates, power purchase agreements, or Guarantees of Origin, which adjust reported emissions without necessarily altering the physical power mix at a specific site.

Location-based vs market-based Scope 2 emission accounting

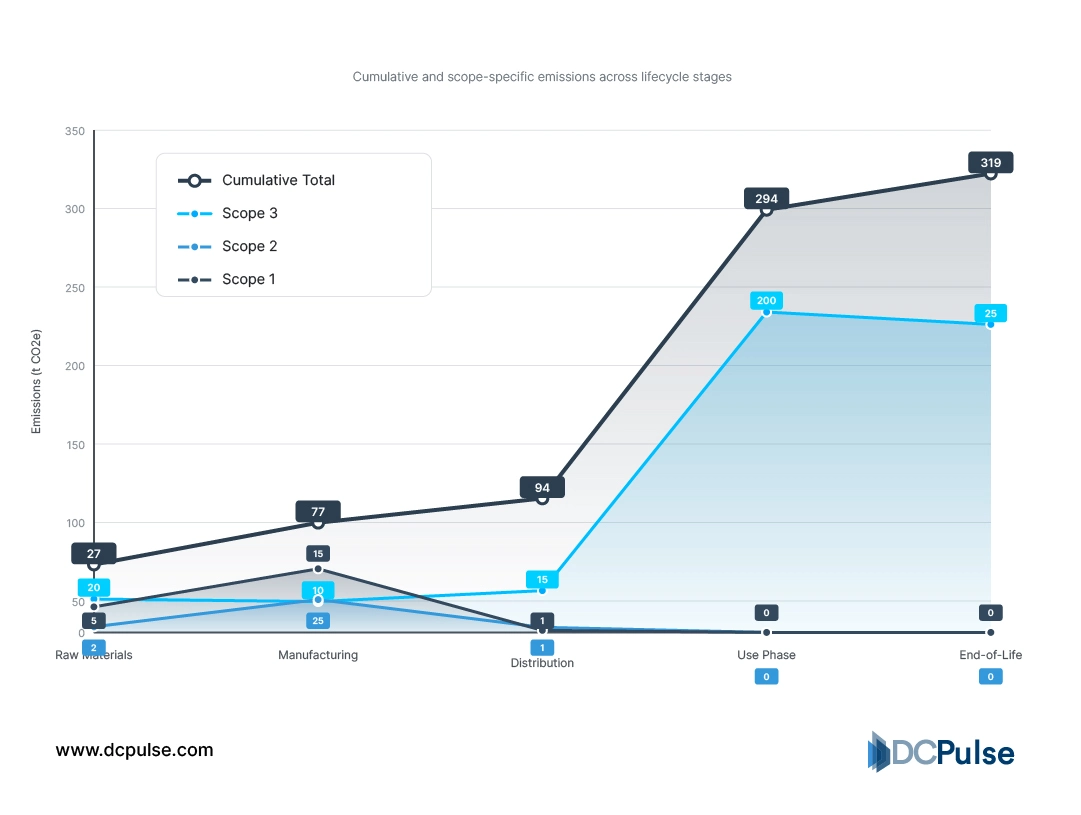

Scope 3 extends beyond daily operations to include emissions embedded in construction materials, IT hardware, and supply chains. Despite often representing the largest share over a facility’s lifecycle, it remains the least consistently measured due to data complexity and limited supplier transparency.

Lifecycle emissions curve highlighting Scope 3 over time

Together, these mechanisms define today’s carbon reporting landscape, effective at standardization but increasingly abstracted from how, when, and where electricity is actually consumed.

Innovations Reshaping Carbon Accounting

Today’s carbon accounting and energy credit systems, while foundational to data center sustainability reporting, are showing their limits as workloads grow, grids tighten, and corporate claims face sharper scrutiny. One of the most significant responses emerging in the industry is a shift from annual or aggregated accounting toward granular, time-matched approaches that more closely mirror real usage and environmental impact.

A major innovation gaining traction is 24/7 carbon-free energy (CFE). Traditional energy credits, such as renewable energy certificates and long-term power purchase agreements (PPAs), have been valuable first steps in helping operators match their annual electricity consumption with renewable generation.

However, they fall short when energy use and clean generation don’t coincide in time or place. The 24/7 CFE approach seeks to match each hour of electricity consumption with carbon-free generation on the same grid, reducing the reliance on offsets and enhancing transparency in reporting.

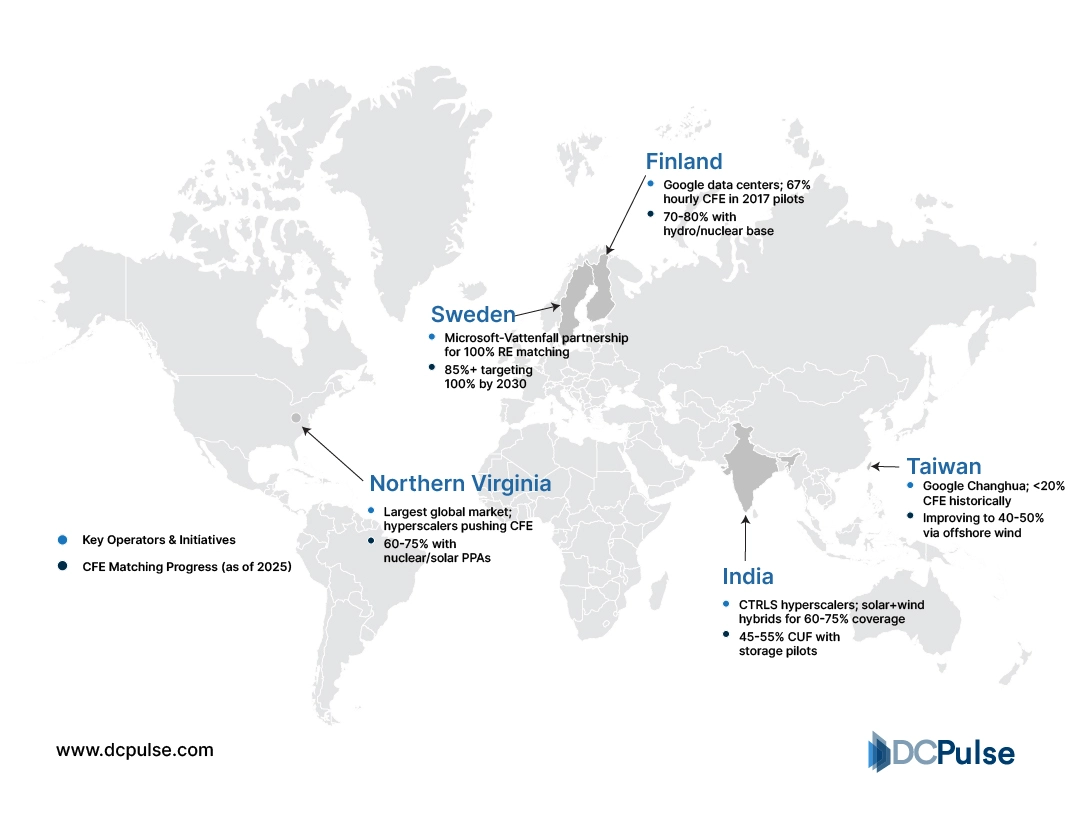

Implementation of hourly matching requires advanced energy tracking and supply strategies, including local procurement of wind, solar, hydro, or other low-carbon sources, energy storage, and real-time metering. Operators such as Iron Mountain and Bulk Data Centers are already piloting or rolling out 24/7 CFE programmes across multiple facilities, pairing detailed consumption data with locally sourced renewable generation.

Data center regions with 24/7 carbon-free energy initiatives

Beyond procurement, emerging tools for traceable energy certification, including blockchain-enabled tracking and time-stamped energy attribute certificates, are starting to surface, aiming to make hourly renewable matching auditable and transparent.

These innovations address core limitations of legacy credits, linking consumption more closely to when and where clean energy is available rather than only on paper, marking an important evolution in data center carbon accounting.

How the Market Is Responding: Real-World Moves in Carbon Strategy

As the limitations of traditional energy credits and annualised carbon reporting become clearer, many data center operators and their customers are adjusting how they source, account for, and disclose emissions. These moves are less about marketing and more about alignment with operational reality and stakeholder expectations.

Hyperscale players have begun shifting toward 24/7 carbon-free energy commitments, which aim to match data center electricity use with carbon-free generation at each hour rather than just on an annual basis. Google, for instance, has publicly committed to powering its global operations with carbon-free energy around the clock by 2030, a strategy that goes beyond conventional RECs and PPAs toward hourly alignment with low-carbon electricity supply.

Across hyperscalers, this evolution is mirrored in emerging frameworks for time-based energy tracking and collaborative clean energy initiatives. Microsoft and partners are investing in aggregated demand models to bring advanced clean electricity projects to market that support more granular, reliable carbon-free supply.

Colocation providers are also adapting by integrating hourly metering and third-party verification into customer disclosures, responding to enterprise demand for transparency in carbon accounting.

Data center markets where enhanced carbon disclosures are becoming procurement requirements

These shifts indicate that the market is moving toward accountability and operational coherence in carbon strategy, linking reported outcomes closer to actual energy sourcing behaviour.

Where Carbon Strategy Is Headed Next?

Energy credits and carbon audits are unlikely to disappear from the data center industry. They remain essential tools for standardisation, benchmarking, and regulatory compliance. What is changing is how much weight they carry on their own.

As data center demand grows, driven by AI, cloud expansion, and regional localisation, the gap between reported carbon performance and physical energy realities is becoming harder to smooth over with annual accounting alone.

The direction of travel is clear. Carbon strategies are moving toward greater temporal, geographic, and operational resolution, with energy procurement, metering, and reporting increasingly linked. Operators that rely solely on certificates and offsets risk falling behind customer expectations, investor scrutiny, and emerging disclosure norms.

For data center leaders, the takeaway is pragmatic rather than ideological. Energy credits are a bridge, not a destination. The most resilient strategies will combine credible accounting with infrastructure, procurement, and transparency choices that reflect how power is actually consumed, hour by hour, region by region.