For most of the last decade, data centers expanded the way capital always has, toward cheap land, friendly tax regimes, and fast-growing metros. Power was assumed. Cooling was engineered. Geography followed demand.

That order has quietly broken.

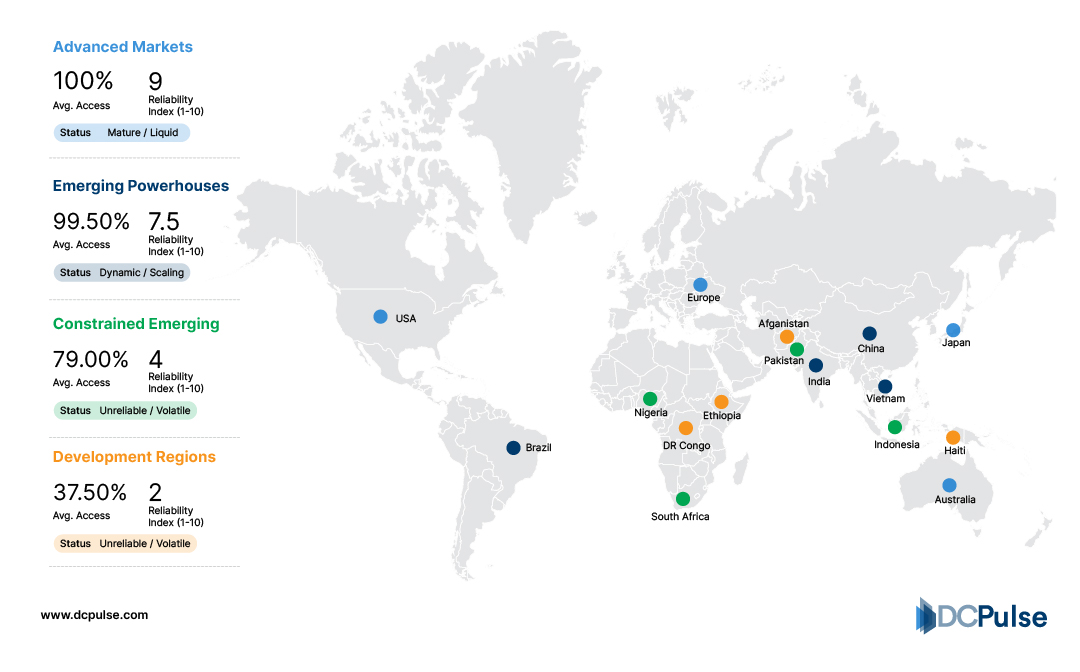

Today, the most valuable data center sites are not where demand is loudest, but where electricity is available, financeable, and predictable over decades. In many mature markets, grid access, not capital, is the scarcest resource. Entire projects stall not because investors hesitate, but because megawatts cannot be secured on realistic timelines.

Private equity has been quicker than most to recognize this shift. As AI workloads push power density higher and planning cycles stretch longer, data centers have stopped behaving like simple real estate assets. They are now energy-first infrastructure platforms, shaped as much by transmission queues and utility balance sheets as by customer contracts.

This is the backdrop against which private equity’s surge into data center ownership should be understood, not as a hunt for yield, but as a recalibration around where infrastructure can still scale.

Capital Meets Constraints: Mapping Today’s Data Centre Investment Landscape

Private equity’s surge into data centers is rooted less in financial fashion and more in how demand, infrastructure risk, and revenue visibility have realigned investor appetites. The explosion of AI workloads and hyperscale cloud capacity has transformed data centers into high-power, long-duration infrastructure platforms, drawing capital that treats them like utilities rather than speculative property.

According to a 2025 investor survey, 95% of global data center investors plan to increase investment this year, with hyperscale development seen as the dominant opportunity.

This shift reflects more than appetite for growth. Power constraints and permitting delays have overtaken debt availability as the primary bottleneck in the sector, underscoring how energy access now drives development feasibility.

Global Energy Landscape: Grid Access vs. Power Constraints (2025)

Private capital’s role is expanding alongside demand. European private capital firms are targeting around EUR 17 billion (~USD 19.92 billion) in data center deals this year, a sign that PE is not just financing existing platforms but actively shaping supply in response to AI-driven demand.

Global Private Equity: Deal Value & Capital Commitments (2021–2025)

.jpg)

At the heart of this landscape are long leases with secured customers, predictable cash flows, and strategic land and power positions, conditions that align tightly with private equity’s return horizons.

In India alone, more than USD 6.5 billion has been invested in the data center sector over the last decade, signifying how global capital is chasing both capacity and future demand growth.

This confluence of AI demand, energy constraint, and long-term contracted revenue defines the current landscape that private equity believes is ripe for infrastructure-scale investment.

How New Designs Enable PEGrade Capacity

Private equity isn’t just financing data centres; it’s helping drive the practical innovations that make next-generation capacity deliverable and investible. As AI workloads push rack power densities far beyond traditional enterprise levels, operators and investors alike are rethinking how facilities are designed, deployed and cooled.

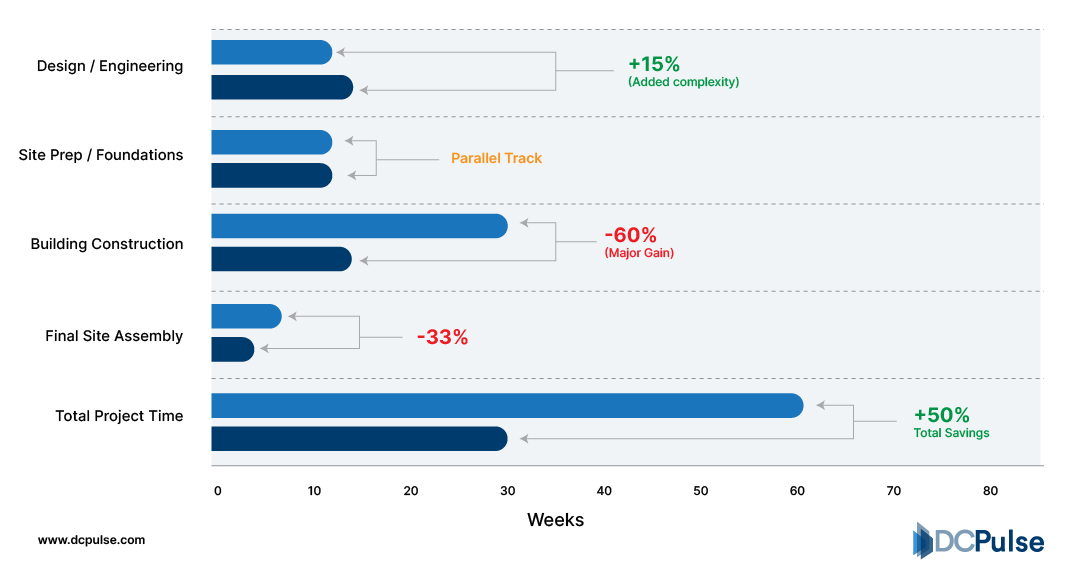

One of the most visible shifts is toward modular and prefabricated infrastructure. These systems allow developers to deploy capacity rapidly, scale in phases, and reduce upfront risk, characteristics that align with private capital’s preference for predictable execution and phased cash flows.

Prefabricated solutions have evolved from simple containerized builds to high-density modules capable of handling AIscale compute, enabling some projects to go from foundation to live capacity much faster than traditional builds.

Modular vs. Traditional Construction: Timeline & Efficiency

At the same time, cooling innovation has shifted from incremental improvement to strategic imperative. Traditional air-based systems struggle with the heat generated by GPUheavy clusters, so operators are deploying advanced thermal solutions, from highdensity liquid cooling to immersion systems, that can reduce energy use and support ultradense racks efficiently. Liquid cooling in particular is gaining ground because it manages heat far more effectively and supports the higher power envelopes that AI compute demands.

Data Center Cooling: Air vs. Liquid Efficiency (2025 Benchmarks)

.jpg)

Innovation around power infrastructure is also critical. As rack density increases, so does stress on the grid and internal distribution systems. Investors and operators are now packaging integrated power and thermal systems, often with on-site generation, storage, or microgrid components, that reduce delivery risk and improve operational resilience. These are not lab concepts; they are being adopted by facilities chasing both speed and sustainability in deployment.

Together, these innovations underpin a new generation of facilities that meet private equity’s need for scalability, mitigated execution risk, and long-term tenant commitment while addressing the technical realities of AI workloads.

Deals, Platforms and the Shape of Concentration

The private equity footprint in data centers isn’t hypothetical, it’s visible in actual, record-setting transactions and platform plays that reveal how capital is concentrating into fewer, larger, future-ready assets.

In 2024 alone, data center M&A hit unprecedented heights, with deals totaling about USD 57 billion and a further USD 16 billion in pending transactions, a scale dwarfing prior years.

Global Data Center M&A Transaction Volume (2018–2024)

.jpg)

One defining move is the planned acquisition of Aligned Data Centers for roughly USD 40 billion by a consortium including BlackRock, Microsoft, Nvidia and others, creating one of the largest data center platforms globally. This deal underscores how PE and institutional capital are willing to underwrite massive, multi-GW infrastructure plays backed by strategic hyperscaler interest.

Deals aren’t limited to mega-acquisitions. Swiss investment firm Partners Group has put up to USD 1.2 billion into EdgeCore Digital Infrastructure to expand U.S. capacity, illustrating mid-sized platform build strategies.

At the same time, firms such as Bain (via Hscale) and Magnetar Capital are actively backing hyperscale platforms and GPU-oriented infrastructure, proving that innovation in investor strategy goes beyond ownership alone to how these assets are capitalized and scaled.

Through record deals, strategic platform investments and capital structures tied to future capacity growth, investors are not only financing but also redefining the competitive landscape of data centers for the coming decade.

What Comes Next for PE-Driven Data Centres

Private equity’s deepening role in data centers is unlikely to slow, but the nature of participation will evolve. As AI demand intensifies, energy access, not capital, will remain the defining constraint, shaping which markets scale and which stall. Investors are already favoring regions and platforms where power can be secured early and expanded predictably, a trend reinforced by industry surveys showing power constraints now outweigh financing risk in mature markets.

At the same time, returns will increasingly hinge on operational differentiation, from advanced cooling to modular expansion strategies that support high-density workloads efficiently. For operators and developers, PE ownership means faster execution expectations, tighter performance discipline, and infrastructure designed for flexibility rather than perfection.

In effect, private equity is no longer just backing data centers; it is helping determine where they get built, how they scale, and which ones remain viable in an energy-constrained, AI-driven future.