Google’s newest investment in Finland has quietly become the clearest signal of a global shift. For years, data-centre builders stayed close to big metros because that’s where the fibre, talent, and enterprise demand lived.

But today, the math looks very different. Land in major cities has become too expensive, power grids are stretched thin, and permits take far too long. So, the industry is moving to places that once sat far outside the spotlight, tier-2 cities that offer cheaper land, faster approvals, cleaner energy, and room to grow.

From the Nordics to the American Midwest, and from India’s smaller tech hubs to emerging Gulf regions, the same pattern keeps showing up; big money is chasing better economics, not bigger skylines.

That’s why Google’s Finland expansion isn’t just a local story, it’s a preview of where the next decade of global data-centre growth is headed.

Why Tier-1 Cities Are Running Out of Space and Power

The economics of data-centre construction are changing fast, and that is pushing developers to look beyond Tier-1 metros. Big hubs like London, Singapore and Northern Virginia face the same problems; expensive land, limited power and slow permits.

At the same time, global demand keeps rising. CBRE says data-centre capacity grew 19% year-on-year in 2024, driven by AI and cloud expansion.

Tier-2 cities are becoming attractive because they offer more space at far better prices. Across global markets, land in secondary cities is often 30-60% cheaper. In the US, primary data-centre land prices have gone up 35–50% since 2021, which is pushing builders to hunt for more affordable plots outside major metros. Cheaper land directly cuts CapEx and allows larger campuses.

Global Industrial Land Cost Inflation Trend (2021–2024)

Power availability is another major reason behind the shift. Several Tier-1 hubs in Europe, including Frankfurt, Amsterdam and Dublin, now have less than 5% grid capacity left for new builds.

Some areas in London even expect no new power allocations until 2035. Tier-2 cities, in contrast, often have more flexible grid connections and shorter waiting times, which helps hyperscalers deploy capacity faster.

Permitting delays add further pressure. In large metros, approvals can take 12-24 months, while Tier-2 cities often finish the same process in 6-9 months. Faster approvals directly cut build time, which matters with AI workloads growing so quickly.

Construction inflation is also reshaping decisions. Turner & Townsend reports global data-centre construction costs rising 8-13% year-on-year, with electrical equipment seeing the biggest increase. Savills notes that a European build can now cost USD 7-13 million per MW, making lower-cost markets far more attractive.

Construction Cost per MW (USD Million)

.jpg)

India shows this shift clearly. Mumbai already ranks among the cheapest global markets at USD 6.64 per watt. With Tier-2 Indian cities offering even lower land and labour costs, developers are rapidly expanding their search.

AI demand will only speed things up. The IEA expects AI training workloads to use 10× more power by 2030, which means builders need cities with space, power flexibility and long-term cost stability, strengths Tier-2 markets naturally offer.

How New Tech Makes Tier-2 Data Centres Work

The biggest shift in Tier-2 data centre growth is driven by new technologies that make it easier, faster and cheaper to build outside traditional hubs. The most visible change is the move toward prefabricated and modular designs, now used by companies like Schneider Electric, Vertiv, Delta, Huawei, ZTE and Eaton.

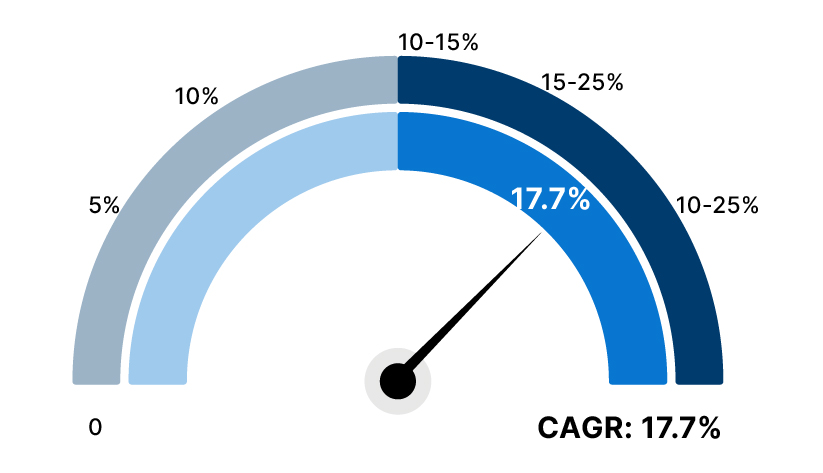

The demand for modular data centres is growing at over 17% CAGR, mainly because hyperscalers want faster build times and predictable costs.

These modular systems cut deployment cycles by 20-40%, a major advantage for Tier-2 cities that lack large construction ecosystems.

Deployment Time Reduction (Traditional build vs Modular build)

.jpg)

Cooling innovation is also reshaping where new facilities can be built. Google, Microsoft, Meta and Amazon are now exploring liquid cooling, immersion systems, and rear-door heat exchangers to manage rising AI power densities.

Advanced cooling can lower energy use by 15-30%, making Tier-2 markets with warmer climates more attractive. A 2024 Uptime Institute study confirms that liquid cooling adoption is accelerating fastest in secondary regions where “cooling efficiency can offset higher grid costs.”

Power is another critical piece. Several Tier-2 cities are gaining attention because of their ability to host on-site renewable energy or long-term clean power contracts. Projects in places like Finland, Spain, Malaysia and the UAE now pair data centres with solar, wind and thermal storage.

Rondo Energy and Enel are working on thermal batteries that can supply stable heat for cooling systems, while Ørsted and EDF are expanding grid-support projects near mid-sized industrial cities. Microsoft recently signed a 10-year clean power agreement in Finland to support new regional builds.

Network infrastructure is improving too. Ciena, Lumen, PCCW Global, Sparkle, Airtel, and Liquid Intelligent Technologies have expanded high-capacity fibre routes across Asia, Africa, and Europe.

Tier-2 cities with upgraded fibre backbones can now offer sub-5 ms latency to nearby metros, removing a major barrier to deployment.

The Big Moves Shaping Tier-2 Data Centres

Big names are already putting money into Tier-2 cities, and their moves are shaping the market.

Google has expanded in Finland, investing heavily in its Hamina campus and buying land for new sites, a clear signal that the company sees value in smaller, cooler Nordic towns.

Microsoft is scaling regional campuses in the U.S. Midwest, with large builds in Iowa that promise thousands of construction hours and long-term jobs.

Amazon continues big pushes in Ohio and other secondary U.S. markets, adding billions in local investment and jobs tied to AWS growth.

Meta keeps expanding outside big metros too, with recent U.S. projects and planned sites that show its preference for large, well-served secondary locations.

On the colocation and network side, Equinix is opening carrier-neutral campuses in cities such as Bordeaux, bringing interconnection to regional markets. Digital Realty’s steady expansions in Dublin show how colocations are following demand into smaller zones.

Major Tier-2 data-centre deals, 2023–2025 (global)

.jpg)

In APAC and India, players like STT GDC and local REITs are growing capacity in Pune and other second-tier hubs, serving domestic cloud and enterprise customers who want lower cost and faster delivery.

What ties these moves together is a common playbook; secure land, lock long-term power deals, and partner with colocation or network providers to get instant interconnect. That approach shortens delivery and lowers risk, exactly what hyperscalers and large colocation buyers need when they scale AI infrastructure quickly.

Why Tier-2 Cities Are the Future of Data Centres?

Tier-2 cities are no longer just alternatives; they are becoming strategic choices for data centre expansion. Cheaper land, faster permitting, and stable power supply make them ideal for hyperscalers, cloud providers, and colocation operators looking to scale AI workloads quickly.

Innovation is key. Prefabricated and modular builds, advanced cooling, and renewable energy integration allow operators to reduce costs and deployment time while meeting sustainability goals. Companies like Google, Microsoft, Delta, and Schneider Electric are already leveraging these approaches to unlock growth outside crowded Tier-1 hubs.

Global demand for AI and cloud services continues to soar. Markets in the US Midwest, Europe’s secondary hubs, and APAC’s expanding tech corridors are poised for rapid capacity growth, supported by fibre network upgrades and renewable power contracts.

For investors and operators, the strategic takeaway is clear: Tier-2 cities offer lower risk, predictable CapEx, and faster time-to-market. The combination of innovation, infrastructure readiness, and supportive local policy positions these cities as the backbone of the next wave of data centre expansion.