Renewable energy is no longer a sustainability add-on for hyperscale data centers; it is becoming a core requirement for scaling digital infrastructure globally.

As demand for cloud and AI services accelerates, hyperscale facilities are consuming unprecedented amounts of electricity. Data centers already account for roughly 1-1.5% of global electricity demand, with hyperscalers representing the fastest-growing segment. This surge is forcing operators to rethink how power is sourced, not just how efficiently it is used.

At the same time, investors, regulators, and customers are increasing pressure on operators to reduce carbon footprints. Renewable energy, particularly solar, wind, and hydro, is emerging as the most scalable path to meet both capacity and sustainability requirements.

But the transition is not straightforward.

Renewables introduce variability, grid dependency, and infrastructure challenges that traditional power models were not designed to handle. As a result, hyperscalers are moving beyond simple energy procurement toward long-term power strategies, including dedicated renewable projects, power purchase agreements, and co-located energy infrastructure.

This creates a defining shift.

Renewable energy is no longer just powering data centers; it is reshaping where and how hyperscale infrastructure is built.

What Defines the Current Landscape of Renewable-Powered Hyperscale Data Centers?

The current landscape of renewable-powered hyperscale data centers is defined by large-scale corporate clean energy procurement dominated by hyperscalers.

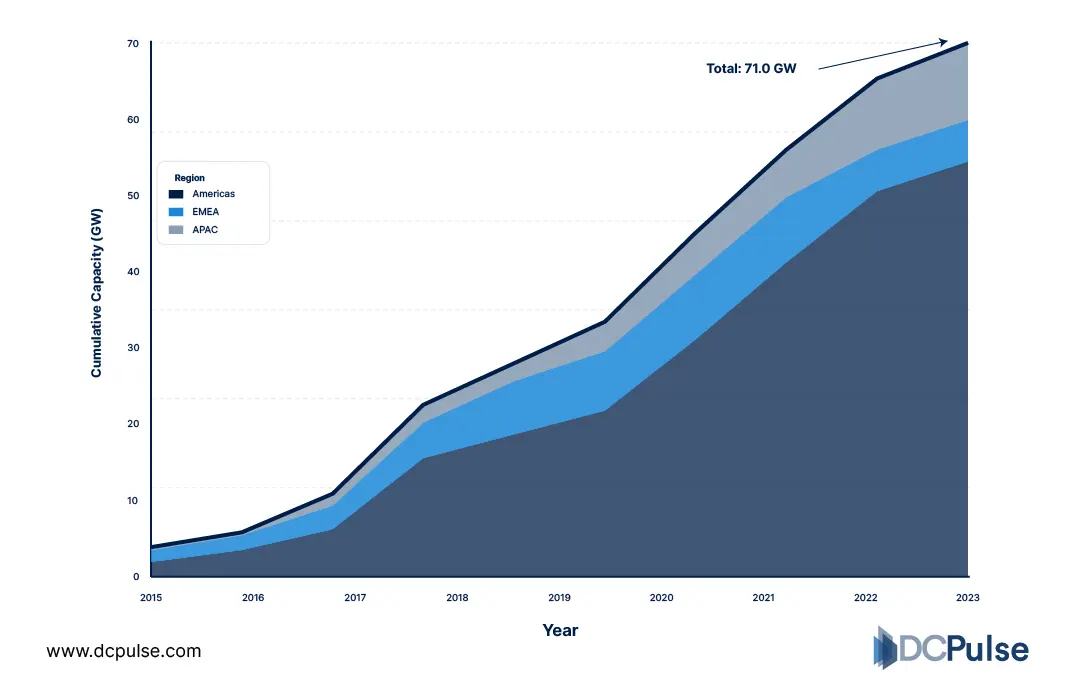

Corporate renewable energy purchasing has reached record levels, with companies signing 46 GW of solar and wind contracts globally in 2023, according to BloombergNEF.

A significant share of this demand comes from large technology firms, where data center expansion is the primary driver.

Global Corporate Renewable Energy Procurement (2015–2023)

This dominance is even more concentrated at the top. In 2025, hyperscalers, including Amazon, Google, Microsoft, and Meta, accounted for ~80% of all corporate renewable energy contracts, highlighting how data center operators are shaping global clean energy markets.

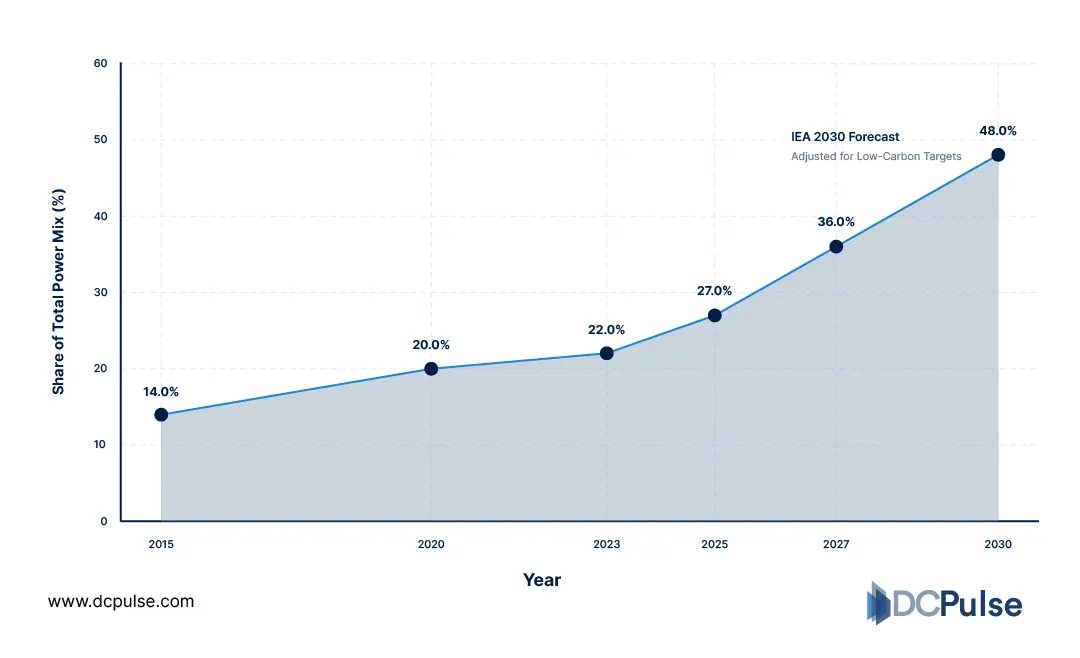

Another defining trend is the rapid increase in renewable energy share within data center operations. According to S&P Global, renewable energy now accounts for ~58% of power sourcing among major data center operators, up from ~50% the previous year.

Renewable Share in Global Data Center Power Mix (%)

Geographically, adoption remains uneven. Most renewable procurement is concentrated in regions with mature energy markets, particularly North America and Europe, where infrastructure and policy frameworks support large-scale PPAs.

The pattern is clear;

Renewable energy is no longer an optional sustainability layer; it has become the primary driver shaping where, how, and at what scale hyperscale data centers are built globally.

How Are Renewable Strategies Evolving Beyond Traditional Procurement?

Renewable strategies in hyperscale data centers are evolving from simple procurement to time-aligned, large-scale, and system-integrated energy models.

A major shift is the move toward 24/7 clean energy matching. Instead of annual renewable offsets, hyperscalers are increasingly aligning electricity consumption with clean energy generation on an hourly basis. This transition is being driven by companies aiming to match demand and supply in real time, moving beyond traditional Power Purchase Agreements (PPAs).

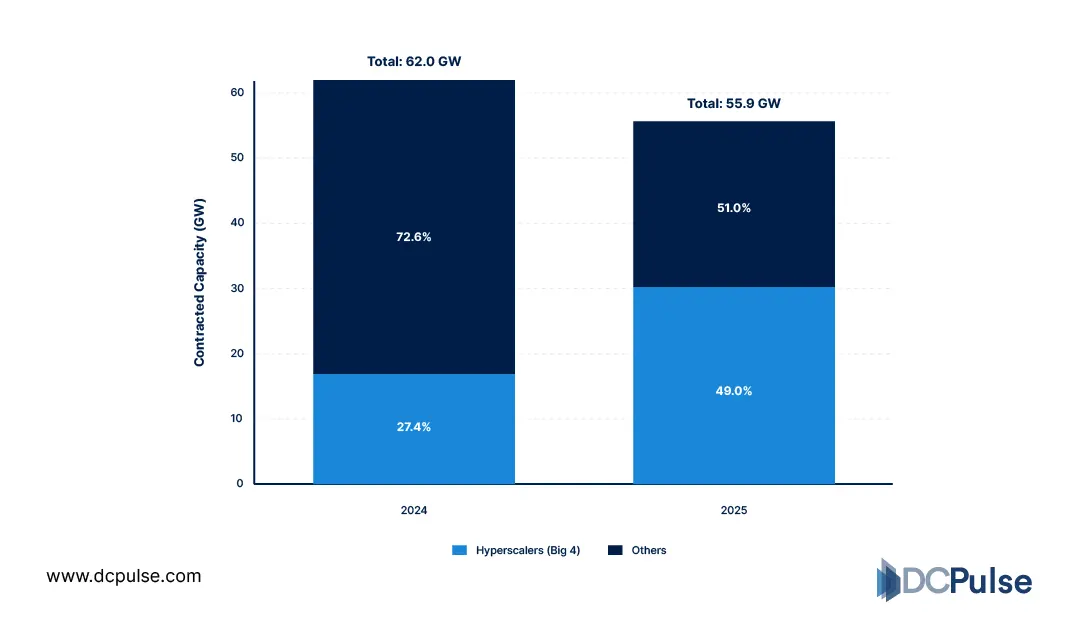

At the same time, the scale and structure of procurement are changing. Hyperscalers are no longer signing isolated contracts; they are securing multi-gigawatt renewable portfolios. In 2025 alone, hyperscalers accounted for ~80% of global corporate renewable energy contracts, highlighting their dominance in shaping clean energy markets.

Share of Renewable Contracts - Hyperscalers vs Others

Another critical evolution is the integration of energy systems with data center infrastructure. Rather than relying purely on grid supply, operators are increasingly combining renewables with storage, long-term PPAs, and flexible energy strategies to manage intermittency and ensure reliability.

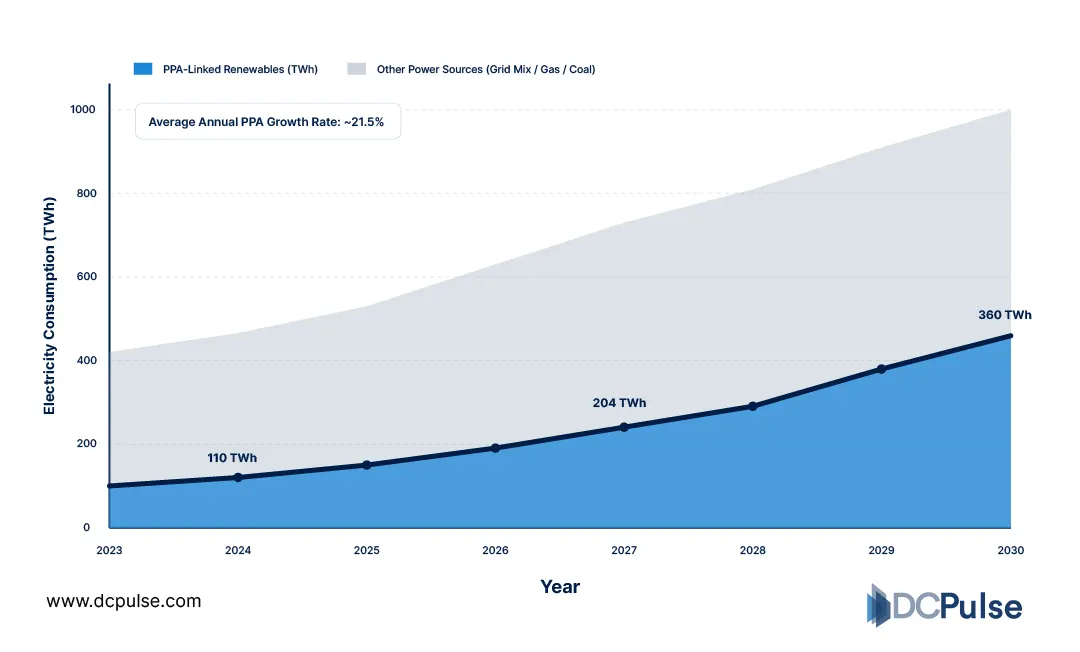

In parallel, renewable procurement is becoming forward-looking and demand-driven. Data centers are expected to contract over 300 TWh/year of PPAs in the coming years, fundamentally reshaping global electricity markets.

Projected PPA Demand & Total Data Center Power (TWh)

The shift is clear;

Renewable strategies are no longer about buying clean energy; they are about engineering energy ecosystems that align generation, storage, and consumption in real time at hyperscale.

Who Is Leading Renewable-Powered Hyperscale Expansion, and What Are They Doing Differently?

The expansion of renewable-powered hyperscale data centers is being led by a small group of companies that are not just consuming energy; they are reshaping global power markets through scale and strategy.

Hyperscalers such as Amazon, Microsoft, Google, and Meta dominate renewable procurement. In 2025, these companies signed 16.7 GW of renewable energy contracts, around 80% of total corporate deals globally, according to S&P Global.

What differentiates these leaders is their shift from procurement to ownership and control of energy supply. Instead of relying only on PPAs, hyperscalers are increasingly investing directly in generation capacity, influencing what type of energy infrastructure gets built.

Key Milestones in Data Center Energy Procurement Evolution

Scale is another defining factor. Major hyperscalers have collectively driven over 45 GW of renewable energy purchases globally, accounting for more than half of the corporate renewables market.

Strategically, renewable energy is no longer just a sustainability initiative; it is tied directly to infrastructure expansion decisions. According to McKinsey & Company, access to carbon-free energy has become a key factor in where and how new data centers are developed.

The shift is clear;

The leaders in hyperscale infrastructure are no longer just technology operators; they are becoming energy market architects, driving investment, influencing grid evolution, and determining how renewable capacity is deployed globally.

Will Renewable Energy Define the Future of Hyperscale Data Centers?

Renewable energy is rapidly shifting from a sustainability priority to a fundamental requirement for hyperscale data center growth.

As demand for AI and cloud infrastructure accelerates, access to large-scale, reliable, and low-carbon power is becoming a defining constraint. Operators can no longer rely solely on traditional grids, particularly in regions where capacity is limited or carbon-intensive. This is pushing renewable energy to the center of long-term infrastructure planning.

However, the transition is not without complexity. Renewable energy introduces variability, requiring new approaches to energy management, including storage, load balancing, and time-based optimization. For many operators, the challenge is no longer securing renewable energy but integrating it effectively into operations.

What is emerging is a structural shift. Data centers are evolving from passive energy consumers into active participants in energy ecosystems, shaping how power is generated, distributed, and consumed.

The direction is clear;

Renewable energy will not just support hyperscale expansion; it will increasingly determine where, how, and at what scale data centers can be built, making it a core driver of future digital infrastructure.