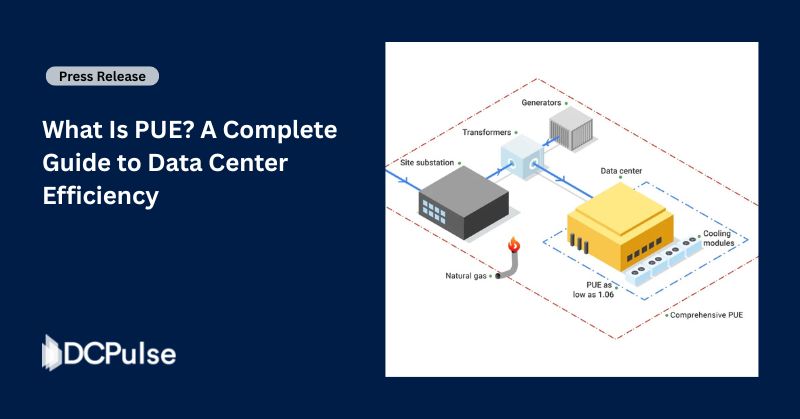

As data center energy demand surges, securing power is no longer just an operational requirement; it is a strategic and financial decision.

To meet sustainability goals and manage long-term energy costs, operators are increasingly turning to renewable energy power purchase agreements (PPAs). These contracts allow data center companies to procure renewable electricity, often from wind or solar projects, at fixed prices over extended periods.

What began as a sustainability initiative has now become a core business strategy.

PPAs provide price stability in volatile energy markets, help meet regulatory and investor expectations, and enable large-scale expansion without relying solely on local grid availability.

At the same time, the scale is unprecedented. Hyperscalers are signing multi-gigawatt renewable deals, effectively becoming some of the largest corporate buyers of clean energy globally.

The result is a structural shift;

Renewable energy PPAs are no longer optional; they are becoming a foundational mechanism for powering and scaling modern data centers, shaping both the economics and sustainability of the industry.

What Does the Current Landscape of Renewable Energy PPAs in Data Centers Look Like?

The current landscape of renewable energy PPAs is defined by record-breaking corporate procurement volumes and rapid scaling driven by large energy consumers such as data centers.

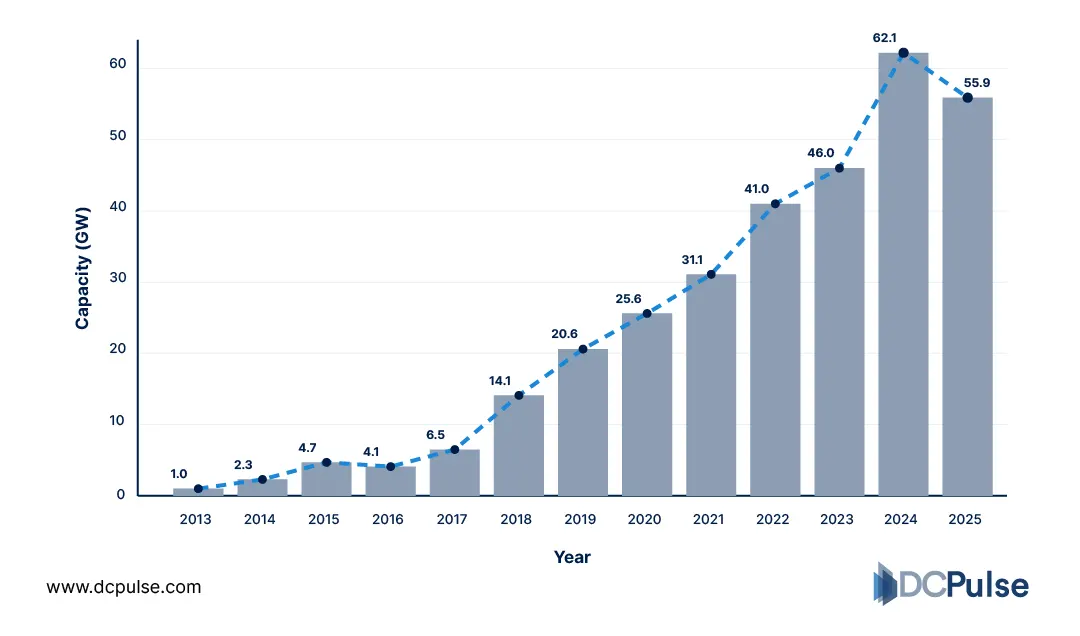

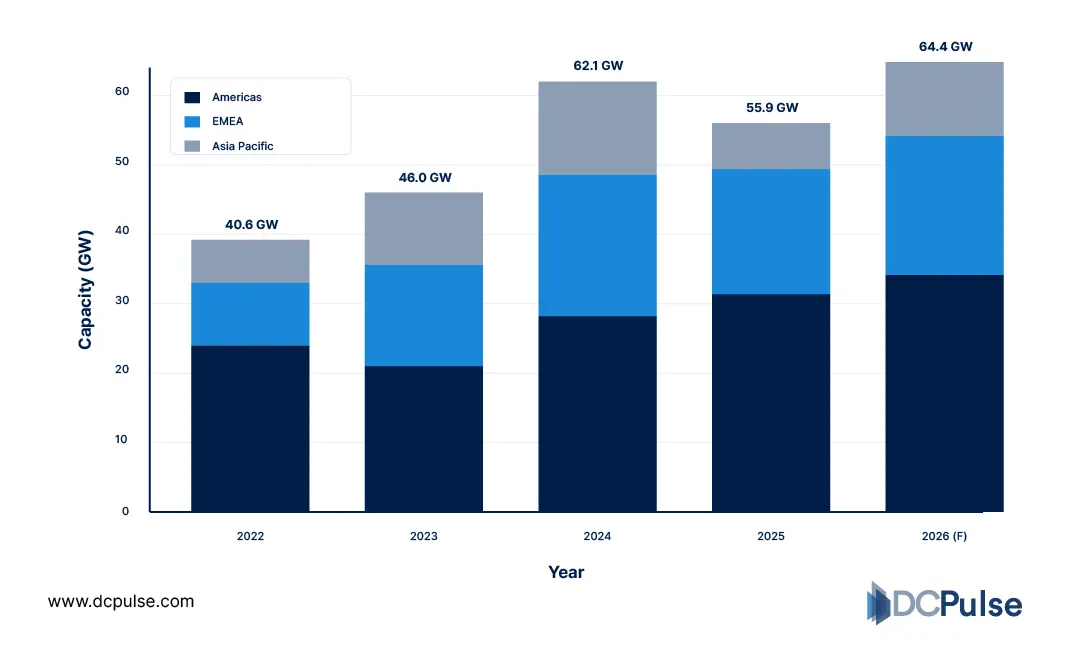

Globally, corporate demand for renewable energy has surged. According to BloombergNEF, corporate PPA volumes reached ~46 GW in 2023, up from 41 GW in 2022, marking a continued upward trend in clean energy contracting.

Global Corporate PPA Volumes (2013-2025)

This growth is being reinforced by sustained deal activity. S&P Global reports that over 30 GW of renewable capacity was contracted in just the first half of 2023, highlighting the accelerating pace of corporate procurement.

At a structural level, PPAs have become a major driver of renewable deployment. Recent analysis indicates that corporate PPAs accounted for around 25% of global wind and solar capacity additions outside China in 2023, a significant increase from just 5% in 2015.

Share of Renewables Driven by Corporate PPAs (%)

Geographically, activity is concentrated in developed markets. North America and Europe dominate PPA adoption, while Asia-Pacific is rapidly expanding as data center growth accelerates in the region.

The pattern is clear;

The current landscape is characterized by large-scale, rapidly growing corporate renewable procurement, with data center operators playing a central role in driving demand and shaping global energy markets.

What Innovations Are Shaping Renewable Energy PPAs for Data Centers?

Renewable energy PPAs are evolving from simple procurement contracts into flexible financial and operational instruments, enabling data centers to better manage cost, geography, and sustainability targets.

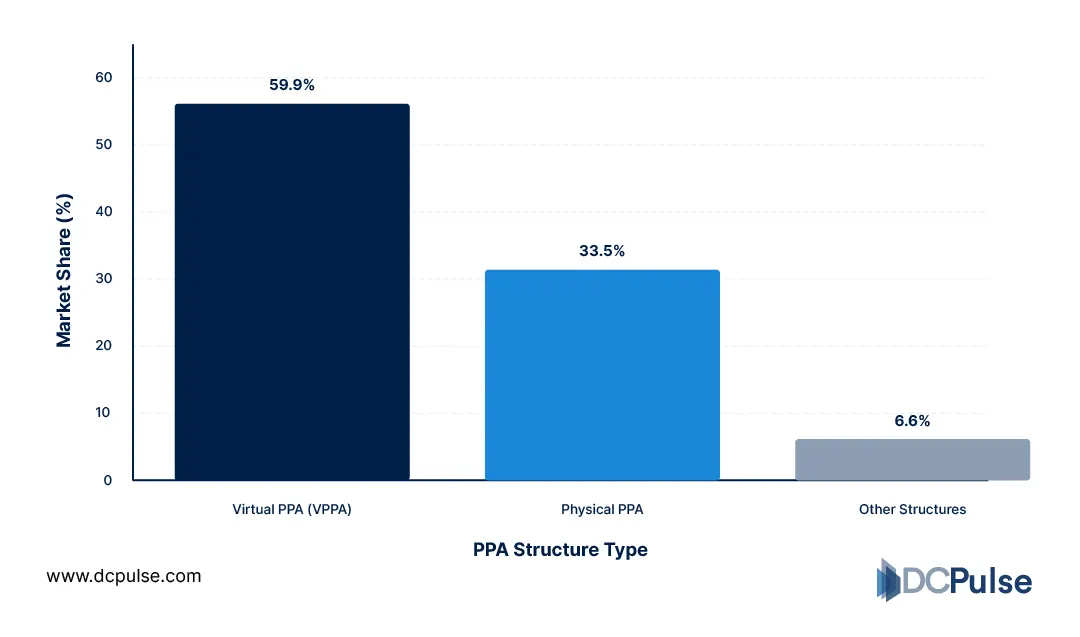

One of the most significant innovations is the rise of virtual power purchase agreements (VPPAs). Unlike traditional PPAs, VPPAs are financial contracts for difference that do not require physical delivery of electricity. Instead, companies secure renewable energy attributes while continuing to draw power from local grids, making them ideal for globally distributed data center operations.

This flexibility has made VPPAs a dominant structure for large corporates operating across multiple regions, where direct physical sourcing is often impractical.

Global Adoption of PPA Structures (2024-2025)

Another key innovation is the shift toward 24/7 clean energy matching. Instead of annual offsets, companies are increasingly aligning renewable generation with actual hourly consumption, improving the accuracy of carbon accounting and pushing more advanced procurement strategies.

In parallel, hybrid and portfolio-based PPAs are emerging. These combine multiple energy sources, such as wind and solar, to balance intermittency and improve reliability, reflecting a more sophisticated approach to energy procurement.

The shift is clear; renewable PPAs are no longer static agreements. They are evolving into dynamic, multi-structured financial tools, enabling data center operators to optimize cost, flexibility, and sustainability in increasingly complex energy markets.

Who Is Leading Renewable Energy PPA Adoption in Data Centers?

The adoption of renewable energy PPAs in data centers is being led by a small group of hyperscale technology companies, whose energy demand and procurement scale far exceed the rest of the industry.

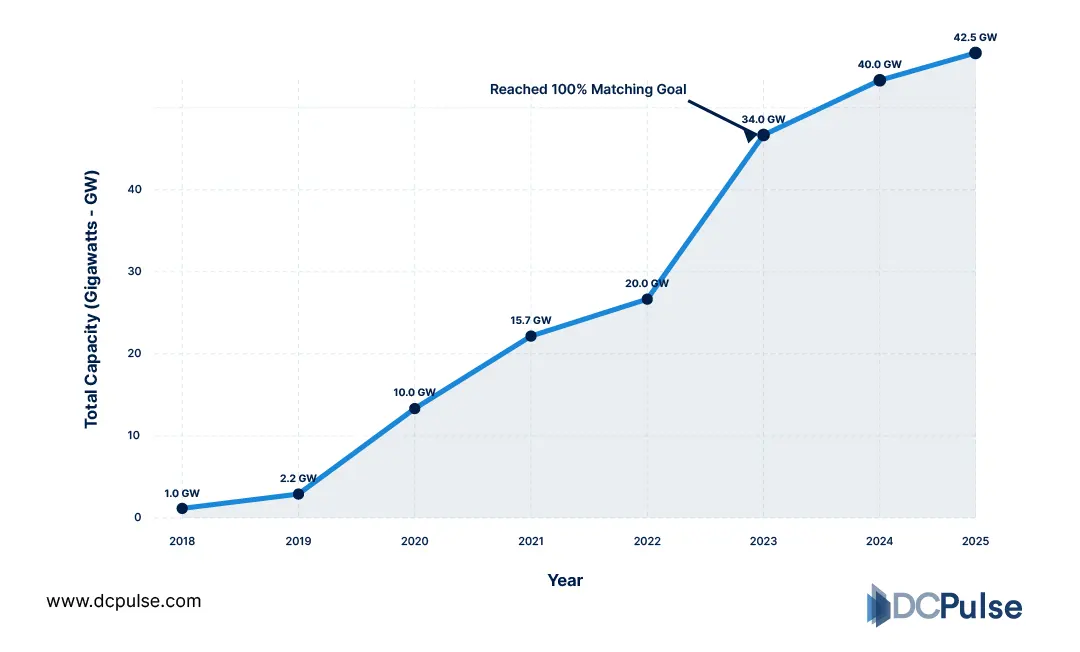

At the forefront is Amazon, which has built the largest corporate renewable energy portfolio globally. The company has contracted over 20 GW of renewable energy capacity across hundreds of projects, primarily to power its global infrastructure, including data centers.

Amazon Global Renewable Energy Capacity Growth (GW)

This leadership is consistent across years. Amazon has remained the largest corporate buyer of renewable energy globally for multiple consecutive years, with investments spanning hundreds of winds and solar projects across multiple countries.

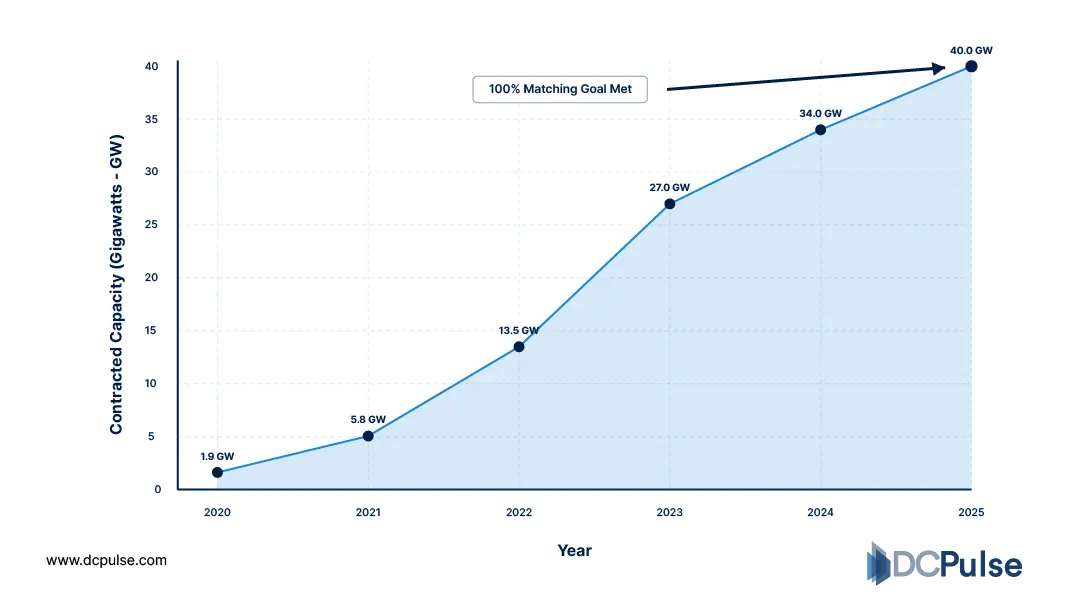

Alongside Amazon, companies like Microsoft are also scaling aggressively. Recent disclosures show Microsoft has contracted around 40 GW of renewable energy globally, using PPAs and other mechanisms to match its electricity consumption and support its data center operations.

Microsoft Cumulative Renewable Energy Procurement (GW)

Similarly, Google continues to expand long-term renewable agreements to support its goal of operating on 24/7 carbon-free energy, including large-scale solar and wind PPAs tied directly to data center demand.

The implication is clear.

Renewable PPA adoption is being driven by a small group of hyperscale leaders, whose massive energy requirements and long-term contractual commitments are not only powering their own data centers but also enabling large-scale renewable energy development globally.

What Will Define the Economics of Renewable PPAs in Data Centers Going Forward?

The economics of renewable PPAs in data centers will be defined by a balance between cost stability, market volatility, and evolving sustainability requirements.

One of the primary advantages of PPAs is long-term price certainty. By locking in electricity prices over 10-20 years, operators can hedge against fluctuations in energy markets, making large-scale data center investments more predictable.

However, this advantage is increasingly influenced by market dynamics. As demand for renewable energy rises, driven in part by data centers, pricing structures are becoming more complex, with variations based on location, grid conditions, and project availability.

At the same time, the shift toward 24/7 clean energy matching and multi-source procurement is changing cost structures. These approaches often require more sophisticated and sometimes more expensive energy portfolios compared to traditional annual matching models.

There is also a growing linkage between PPAs and infrastructure expansion. Access to renewable energy is becoming a site selection factor, directly influencing where new data centers are built.

The direction is clear;

Renewable PPAs will remain central to data center strategy, but their value will increasingly depend on how effectively operators balance cost, flexibility, and sustainability in a rapidly evolving energy landscape.