For years, IT operations focused on what they could measure directly: power draw, cooling efficiency, rack density, utilization rates. Scope 1 and Scope 2 emissions, fuel burned on-site, and electricity consumed became part of sustainability dashboards and annual reports.

But Scope 3 is different.

Scope 3 emissions do not come from the data center floor. They come from everything surrounding it: server manufacturing, semiconductor fabrication, logistics chains, upstream suppliers, third-party colocation providers, cloud vendors, hardware disposal, and embodied carbon locked into infrastructure before it is ever powered on.

And in many technology organizations, Scope 3 accounts for the majority of total emissions.

That means the largest portion of an IT operation’s carbon footprint is embedded in procurement decisions, vendor relationships, and lifecycle strategy, not in power meters.

Tracking Scope 3 is no longer an ESG reporting exercise. It is becoming a visibility problem inside the infrastructure strategy. The operators who can measure embodied and supply-chain emissions will shape procurement standards, vendor negotiations, and capital allocation. Those who cannot will inherit carbon risk they do not see.

Scope 3 turns sustainability into a supply-chain intelligence challenge.

And for IT operations, that changes everything.

The Visibility Gap Inside IT Supply Chains

Most IT teams can measure electricity consumption down to the rack. Very few can quantify the carbon embedded in the equipment inside it.

Under the Greenhouse Gas Protocol, Scope 3 includes upstream emissions from purchased goods and services, which, for IT operations, primarily means servers, storage systems, networking gear, and the semiconductor supply chain behind them.

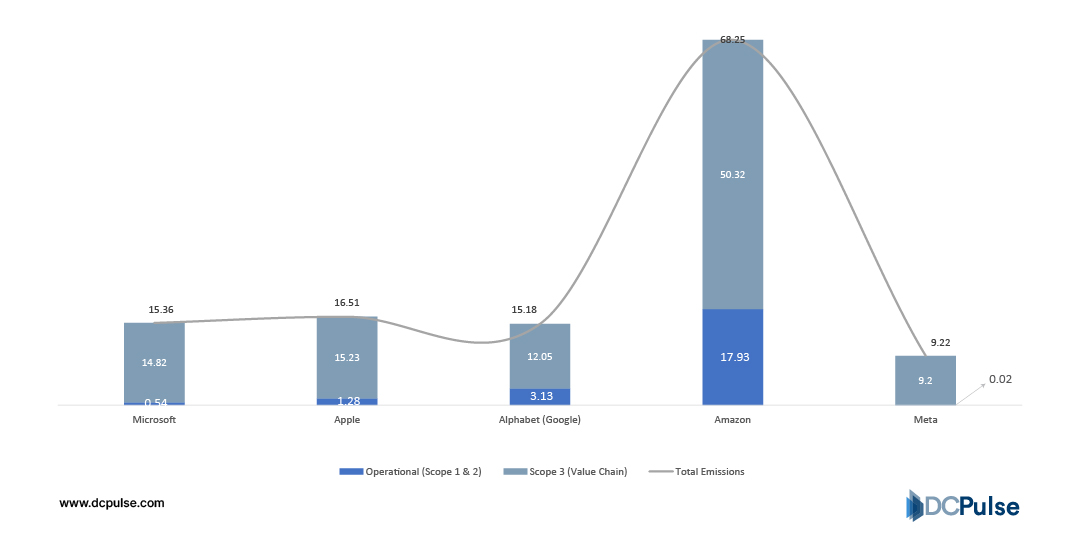

For technology companies, these indirect emissions are often dominant. Apple reports that over 70% of its total carbon footprint comes from product manufacturing and supply chain activity rather than operational energy use.

Similarly, Microsoft discloses that Scope 3 emissions represent the majority of its total reported footprint, largely driven by purchased goods and capital equipment.

Emissions Breakdown of Major Tech Firms (2025)

The challenge is structural. Hardware vendors report carbon intensity at the product or corporate level, not per deployment configuration. Colocation providers disclose facility-level efficiency metrics like PUE but rarely include embodied carbon in construction materials or tenant-specific lifecycle impact.

The result is a visibility gap. IT operators are accountable for emissions that originate far beyond their control plane, yet increasingly must report and justify them.

That tension defines the current landscape.

From Reporting to Measurable Infrastructure Carbon

What is changing is not the definition of Scope 3; it is the instrumentation around it.

Cloud providers have begun exposing carbon visibility directly through customer dashboards. Microsoft offers its Emissions Impact Dashboard to quantify emissions associated with Azure usage. Google provides Carbon Footprint reporting for Google Cloud customers, translating infrastructure consumption into emissions estimates. These tools do not eliminate Scope 3, but they introduce machine-readable accounting into operational workflows.

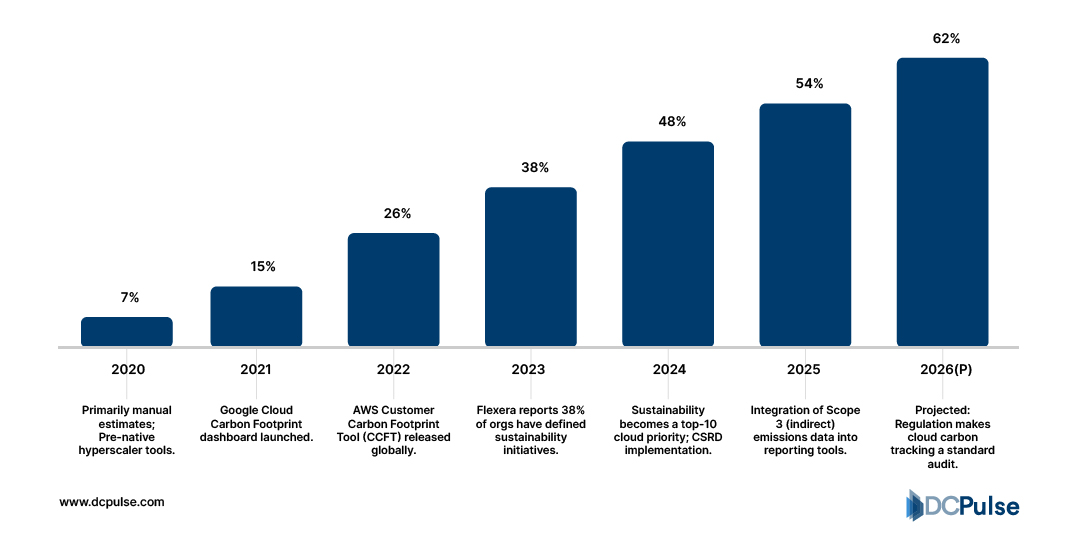

Enterprise Adoption of Cloud Carbon Reporting Tools (2020–2026)

Hardware manufacturers are moving in parallel. Dell Technologies now publishes product-level carbon footprints for select systems, detailing embodied emissions across lifecycle stages. This allows procurement teams to compare infrastructure not only on performance and price but also on embodied carbon intensity.

Meanwhile, lifecycle assessment standards continue to formalize measurement frameworks under ISO 14040 and related environmental management standards, enabling more consistent product-level disclosures across suppliers.

The shift is subtle but significant. Carbon accounting is moving from annual sustainability reports into operational decision systems.

Scope 3 is becoming computable, not just declarable.

Regulation and Procurement Are Forcing the Issue

Scope 3 tracking is no longer voluntary optics. Regulation and investor pressure are pushing emissions disclosure deeper into supply chains.

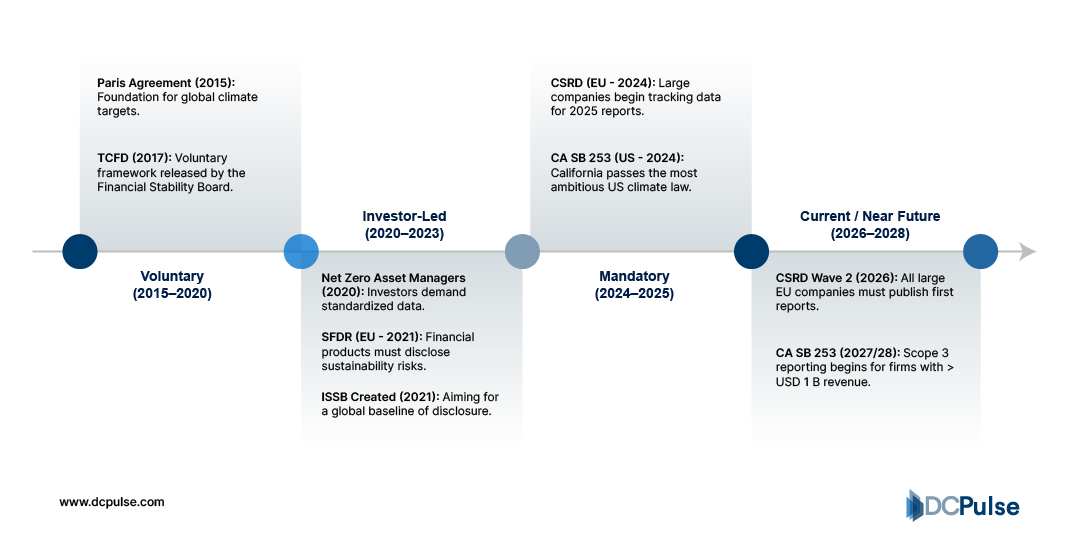

In the United States, the U.S. Securities and Exchange Commission finalized climate disclosure rules in 2024 requiring publicly traded companies to report climate-related risks and material emissions data, including Scope 3 when deemed material. In Europe, the European Commission Corporate Sustainability Reporting Directive (CSRD) expands mandatory sustainability reporting across thousands of companies, explicitly covering value-chain emissions.

Evolution of Climate Disclosure (2015-2028)

Hyperscalers are responding upstream. Amazon has committed to net-zero carbon by 2040 under The Climate Pledge, requiring suppliers to report and reduce emissions. Microsoft has pledged to be carbon negative by 2030 and to address Scope 3 emissions across its supply chain.

The effect cascades downward. When large cloud buyers demand emissions transparency, OEMs, semiconductor manufacturers, logistics providers, and colocation operators are pulled into standardized reporting frameworks.

Scope 3 is no longer a sustainability department metric. It is becoming a procurement condition.

From Carbon Reporting to Supply-Chain Intelligence

The next phase of Scope 3 in IT operations will not be about reporting accuracy. It will be about competitive leverage.

As emissions data becomes standardized and machine-readable, procurement teams will begin comparing infrastructure vendors not only on cost, density, and performance but also on embodied carbon per workload deployed. Carbon intensity will become another performance metric, particularly for enterprises facing disclosure pressure under evolving regulatory frameworks.

Over time, three structural shifts are likely.

First, carbon data will integrate directly into IT asset management systems and ERP platforms, transforming lifecycle planning into a dual optimization problem: cost efficiency and carbon efficiency.

Second, supplier contracts will increasingly require product-level emissions disclosure. Vendors unable to provide defensible lifecycle data risk exclusion from enterprise frameworks.

Third, colocation and cloud providers will compete on transparency, not just renewable energy procurement. Facility-level PUE will no longer be sufficient; tenants will ask for construction materials data, embodied emissions, and hardware sourcing disclosures.

Scope 3 began as an accounting category. It is becoming a systems-level visibility challenge.

For IT operations, the organizations that can quantify supply chain carbon with the same precision they measure power usage will define the next standard of infrastructure accountability and, increasingly, market preference.